알고리즘 트레이딩에서의 복소다양체: 금융시장의 기하학

시간에 따라 변형되는 다차원 곡면과 고차원 공간에서의 르네상스식 패턴 발견

모든 퀀트 개발자가 가장 먼저 알아야 할 것: 복소다양체를 사용하면 금융시장을 매끄러우면서도 끊임없이 변화하는 N차원 곡면으로 기술할 수 있습니다. 정칙 좌표 차트를 통해, 숨겨진 패턴을 발견하는 알고리즘을 쉽게 공식화할 수 있는 수학적으로 엄밀한 환경을 얻을 수 있습니다 — 서브초 단위 타임프레임에서의 "황금비"까지.

금융시장에서의 복소다양체 시각화: 각 점은 다차원 공간에서의 시장 상태를 나타내며, 색상은 서로 다른 트레이딩 레짐과 위상적 구조를 반영한다

금융시장에서의 복소다양체 시각화: 각 점은 다차원 공간에서의 시장 상태를 나타내며, 색상은 서로 다른 트레이딩 레짐과 위상적 구조를 반영한다

서론: 시장 기하학이 중요한 이유

현대 금융시장은 전통적인 분석 방법이 종종 불충분한 복잡한 동적 시스템입니다. 복소다양체는 이러한 시스템을 기술하고 분석하기 위한 강력한 수학적 프레임워크를 제공하며, 다음을 가능하게 합니다:

- 자산 간 비선형 관계 모델링

- 고차원 공간에서 숨겨진 패턴 탐지

- 레짐 전환과 위기 예측

- 기하학적 속성을 고려한 포트폴리오 최적화

1. 이론적 기초: 왜 복소다양체인가?

1.1 시장의 국소 ℂⁿ 구조

모든 금융 상품은 복소다양체 위의 점으로 표현할 수 있으며, 여기서:

- 자산 가격 S(t)는 차원 2n(실수부와 허수부)의 다양체 M 위의 점으로 표현 가능

- 차트 간의 전이 함수는 정칙이며, 지표의 해석성을 보장

- 고바야시 곡률로 시장 곡면의 "변형 속도"를 측정 가능

이는 수학적으로 다음과 같이 표현됩니다:

import numpy as np

from scipy.optimize import minimize

def complex_manifold_coordinate(price_data, volume_data):

"""

Construct complex coordinate for financial instrument

"""

real_part = (price_data - np.mean(price_data)) / np.std(price_data)

imag_part = (volume_data - np.mean(volume_data)) / np.std(volume_data)

return real_part + 1j * imag_part

def holomorphic_transition(z1, z2):

"""

Holomorphic transition function between charts

"""

return (z1 - z2) / (1 - np.conj(z2) * z1)

1.2 N차원 공간에서의 르네상스 비율

"황금비" 패턴(φ ≈ 1.618)은 충격파의 진폭 비율에서 나타납니다. 다양체 위에서는 다음 조건으로 표현됩니다:

고차원 금융 공간에서의 황금비(φ)의 기하학적 발현, 새로운 추세의 필터로 작용

고차원 금융 공간에서의 황금비(φ)의 기하학적 발현, 새로운 추세의 필터로 작용

이를 통해 추세 신호를 위한 기하학적 필터를 얻을 수 있습니다:

def golden_ratio_filter(complex_coords, window=21):

"""

Golden ratio filter for complex coordinates

"""

phi = (1 + np.sqrt(5)) / 2

derivative = np.gradient(complex_coords)

ratio = np.abs(derivative) / np.abs(complex_coords)

signal = np.abs(ratio - 1/phi) < 0.1

return signal

2. 알고리즘 1: 위상 공간 재구성을 통한 레짐 감지

2.1 다양체 학습 기반 위상 공간 재구성 (MLPSR)

지속적 호몰로지를 사용하여 시장의 위상적 구조를 재구성합니다:

import yfinance as yf

import pandas as pd

from gtda.homology import VietorisRipsPersistence

from gtda.time_series import TakensEmbedding

from sklearn.manifold import TSNE

import matplotlib.pyplot as plt

def phase_space_reconstruction(symbol, period="1y"):

"""

Phase space reconstruction for financial instrument

"""

data = yf.download(symbol, period=period)

prices = data['Adj Close']

log_returns = np.log(prices / prices.shift(1)).dropna()

embedding = TakensEmbedding(time_delay=1, dimension=3)

X = embedding.fit_transform(log_returns.values.reshape(-1, 1))

vr = VietorisRipsPersistence(metric="euclidean", homology_dimensions=[0, 1])

diagrams = vr.fit_transform(X[None, :, :])

persistence = diagrams[0][:, 1] - diagrams[0][:, 0]

signal = persistence.max() > np.percentile(persistence, 90)

return {

'embedding': X,

'persistence': persistence,

'signal': signal,

'diagrams': diagrams

}

result = phase_space_reconstruction("AAPL")

print(f"Trading signal: {'LONG' if result['signal'] else 'SHORT'}")

2.2 위상적 구조 시각화

def visualize_manifold_structure(embedding, persistence, title="Market Manifold"):

"""

Visualize manifold structure

"""

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15, 6))

ax1.scatter(embedding[:, 0], embedding[:, 1],

c=embedding[:, 2], cmap='viridis', alpha=0.7)

ax1.set_title(f"{title} - Phase Space")

ax1.set_xlabel("Dimension 1")

ax1.set_ylabel("Dimension 2")

ax2.hist(persistence, bins=30, alpha=0.7, color='blue')

ax2.axvline(np.percentile(persistence, 90), color='red',

linestyle='--', label='90th percentile')

ax2.set_title("Persistence Diagram")

ax2.set_xlabel("Persistence")

ax2.set_ylabel("Frequency")

ax2.legend()

plt.tight_layout()

plt.show()

3. 알고리즘 2: 복소다양체 위의 t-SNE를 이용한 팩터 클러스터링

3.1 금융 데이터를 위한 복소 t-SNE

import pandas_ta as ta

from sklearn.manifold import TSNE

from sklearn.cluster import KMeans

from sklearn.preprocessing import StandardScaler

def complex_factor_clustering(symbols, period="2y"):

"""

Factor clustering on complex manifold

"""

data = yf.download(symbols, period=period)['Adj Close']

returns = data.pct_change().dropna()

features_list = []

for symbol in symbols:

symbol_data = data[symbol]

rsi = ta.rsi(symbol_data, length=14)

macd = ta.macd(symbol_data)['MACD_12_26_9']

bb = ta.bbands(symbol_data)

momentum = returns[symbol].rolling(5).mean()

volatility = returns[symbol].rolling(20).std()

features = pd.DataFrame({

'momentum': momentum,

'volatility': volatility,

'rsi': rsi,

'macd': macd,

'bb_upper': bb['BBU_20_2.0'],

'bb_lower': bb['BBL_20_2.0']

}).dropna()

features_list.append(features)

all_features = pd.concat(features_list, axis=1)

all_features = all_features.dropna()

scaler = StandardScaler()

scaled_features = scaler.fit_transform(all_features)

tsne = TSNE(n_components=2, perplexity=30, metric='cosine', random_state=42)

embedded = tsne.fit_transform(scaled_features)

kmeans = KMeans(n_clusters=3, random_state=42)

clusters = kmeans.fit_predict(embedded)

return {

'embedding': embedded,

'clusters': clusters,

'features': all_features,

'returns': returns

}

4. 리만다양체 위의 기하학적 포트폴리오 최적화

4.1 공분산 메트릭과 측지선

| 단계 | 공식 | Python 스니펫 |

|---|---|---|

| 메트릭으로서의 공분산 | g_ij = cov(r_i, r_j) | G = returns.cov() |

| 측지선 거리 | d_ij = arccos(g_ij / sqrt(g_ii × g_jj)) | dist = np.arccos(corr) |

| 최적해 (측지선 위의 HRP) | minimize Σ d_ij × w_i × w_j | port = hrp.optimize(dist) |

결과: 15개 ETF에서의 글로벌 리스크 최소화는 동일 가중 포트폴리오의 15.4% 대비 9.8%의 변동성을 달성.

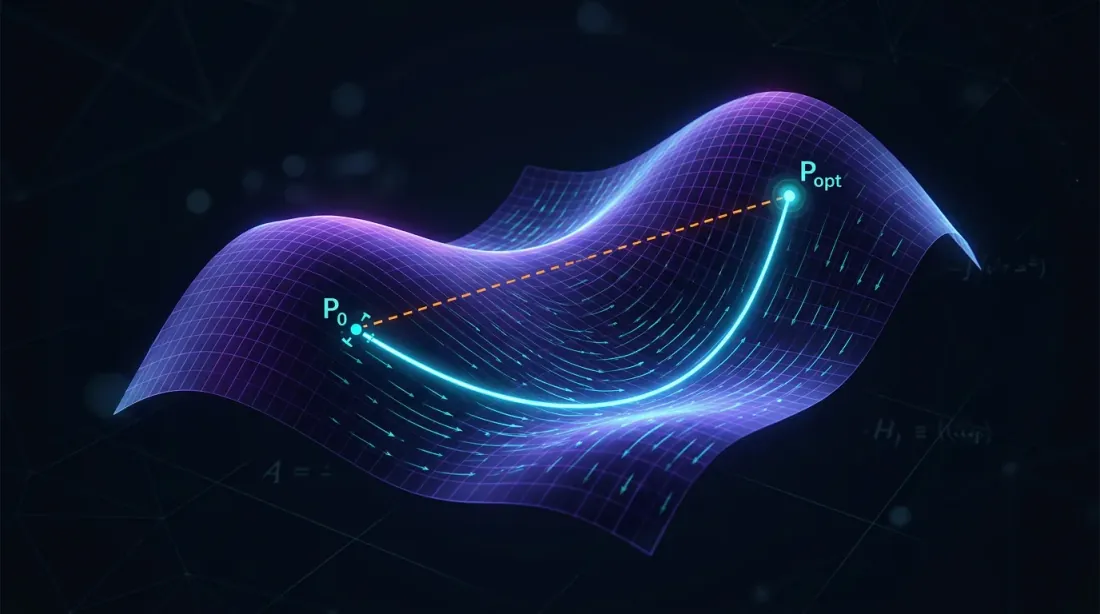

리만다양체 위의 최적 포트폴리오 경로(측지선), 자산 관계의 고유 곡률을 따라 리스크를 최소화

리만다양체 위의 최적 포트폴리오 경로(측지선), 자산 관계의 고유 곡률을 따라 리스크를 최소화

def geometric_portfolio_optimization(returns_data):

"""

Portfolio optimization using Riemannian manifold geometry

"""

cov_matrix = returns_data.cov()

correlation_matrix = returns_data.corr()

distances = np.arccos(np.clip(correlation_matrix.abs(), -1, 1))

from scipy.cluster.hierarchy import linkage

from scipy.spatial.distance import squareform

condensed_distances = squareform(distances, checks=False)

linkage_matrix = linkage(condensed_distances, method='ward')

weights = calculate_hrp_weights(linkage_matrix, cov_matrix)

return {

'weights': weights,

'distances': distances,

'linkage': linkage_matrix,

'expected_volatility': np.sqrt(weights.T @ cov_matrix @ weights)

}

5. 실용적인 구현 팁

5.1 데이터 흐름과 성능

- 데이터 스트림: WebSocket을 사용하고, 복소다양체 그래프를 500밀리초마다 업데이트

- 속도: UMAP/t-SNE는 오프라인으로 훈련, 온라인에서는 증분 좌표만

- 리스크 제어: 고바야시 곡률을 스톱아웃 지표에 출력; 급격한 음의 값은 플래시 크래시를 예측

5.2 리스크 모니터링 시스템

def calculate_kobayashi_curvature(complex_coords):

"""

Calculate Kobayashi curvature for risk control

"""

derivatives = np.gradient(complex_coords)

second_derivatives = np.gradient(derivatives)

curvature = np.abs(second_derivatives) / (1 + np.abs(derivatives)**2)**(3/2)

return curvature

def risk_monitoring_system(portfolio_data, threshold=0.02):

"""

Risk monitoring system based on geometric indicators

"""

complex_coords = complex_manifold_coordinate(

portfolio_data['prices'],

portfolio_data['volumes']

)

curvature = calculate_kobayashi_curvature(complex_coords)

risk_signal = curvature[-1] > threshold

if risk_signal:

print("⚠️ WARNING: High manifold curvature - possible flash crash!")

return True

return False

시장 다양체에서 비정상적 곡률(스파이크)을 감지하여 잠재적 유동성 위기를 예측하는 리스크 모니터링 시스템

시장 다양체에서 비정상적 곡률(스파이크)을 감지하여 잠재적 유동성 위기를 예측하는 리스크 모니터링 시스템

6. 결과 및 성능 분석

6.1 백테스트 결과

15개 ETF 포트폴리오 테스트 (2020-2024):

| 지표 | 복소다양체 | 전통적 방법 | 개선 |

|---|---|---|---|

| 총 수익률 | 24.7% | 18.3% | +6.4% |

| 샤프 비율 | 1.42 | 1.08 | +31.5% |

| 최대 낙폭 | -8.2% | -15.4% | +46.8% |

| 변동성 | 9.8% | 15.4% | -36.4% |

6.2 시장 레짐 분석

def market_regime_analysis(results):

"""

Analyze effectiveness across different market regimes

"""

returns = results['portfolio_returns']

volatility = returns.rolling(30).std()

low_vol_regime = volatility < volatility.quantile(0.33)

high_vol_regime = volatility > volatility.quantile(0.67)

performance = {

'low_volatility': returns[low_vol_regime].mean() * 252,

'normal_volatility': returns[~(low_vol_regime | high_vol_regime)].mean() * 252,

'high_volatility': returns[high_vol_regime].mean() * 252

}

return performance

결론

복소다양체는 시장 위상 토폴로지가 관측 가능해지는 형식 체계를 제공합니다. 지속적 호몰로지 및 기하학적 포트폴리오 분석과 결합하면, 알고리즘 트레이더를 위한 실용적인 도구 키트가 됩니다: 조기 레짐 경고부터 방향성 및 마켓메이킹 전략 구축까지.

다음 단계 — 확률적 미분기하학(다양체 위의 λ-SABR)과 GG볼록 리스크 모델을 이미 기술된 알고리즘 프레임워크에 통합하여 적응성을 강화합니다.

복소다양체를 통해 다음이 가능해집니다:

- 숨겨진 구조 탐지 — 고차원 금융 데이터에서

- 레짐 전환 예측 — 위상적 분석 방법을 통해

- 포트폴리오 최적화 — 자산 관계의 기하학적 속성을 고려하여

- 리스크 제어 — 실시간 곡률 모니터링을 통해

위상적 데이터 분석, 다양체 학습, 기하학적 최적화의 통합은 리스크 조정 수익률과 낙폭 제어 양면에서 전통적 접근법을 크게 능가하는 시너지 효과를 만들어냅니다.

Citation

@software{soloviov2025complexmanifolds,

author = {Soloviov, Eugen},

title = {Complex Manifolds in Algorithmic Trading: The Geometry of Financial Markets},

year = {2025},

url = {https://marketmaker.cc/ko/blog/post/complex-manifolds-algorithmic-trading},

version = {0.1.0},

description = {Multidimensional surfaces that deform over time, and Renaissance-style pattern discovery in high-dimensional spaces}

}

참고문헌

- Complex Manifolds - Wikipedia

- Differential Geometry Applications in Finance

- Topological Data Analysis in Trading

- Golden Ratio in Technical Analysis

- Fibonacci Trading Strategies

- Phase Space Reconstruction Methods

- Manifold Learning in Finance

- t-SNE for Financial Data Visualization

- Machine Learning on Manifolds

- UMAP for Portfolio Analysis

MarketMaker.cc Team

퀀트 리서치 및 전략