อาร์บิทราจ Funding Rate ข้ามกระดาน: วิธีทำกำไรจากความแตกต่างของอัตรา

Funding rate ของ ETHUSDT อยู่ที่ 0.01% บน Binance และ 0.035% บน Bybit เหรียญเดียวกัน ช่วงเวลาเดียวกัน แต่อัตราต่างกันถึง 3.5 เท่า บางคนจ่ายมากกว่า บางคนจ่ายน้อยกว่า และมีคนที่ทำกำไรจากความแตกต่างนี้

อาร์บิทราจ Funding Rate เป็นหนึ่งในไม่กี่กลยุทธ์ใน crypto ที่ไม่ขึ้นอยู่กับทิศทางของตลาด คุณไม่ต้องทำนายราคา คุณดึงกำไรจากความแตกต่างเชิงโครงสร้างของอัตราระหว่างกระดาน

ทำไม Funding Rate จึงแตกต่างกันระหว่างกระดาน

Funding rate คือกลไกที่ยึดราคาสัญญา perpetual futures ให้ใกล้เคียงกับราคา spot แต่ละกระดานคำนวณแยกจากกันโดยใช้ข้อมูลของตัวเอง:

- องค์ประกอบของนักเทรด Binance มีนักเทรดรายย่อยครองตลาด ซึ่งมักจะ long Bybit และ OKX มีผู้เข้าร่วมมืออาชีพมากกว่า ความสมดุล long/short ที่ต่างกันนำไปสู่ funding ที่ต่างกัน

- สูตรการคำนวณ แต่ละกระดานใช้สูตรของตัวเอง Binance คำนวณจาก premium index และ interest rate Bybit และ OKX ใช้แนวทางเดียวกันแต่ต่างน้ำหนักและช่วงเวลาเฉลี่ย

- สภาพคล่อง บนกระดานที่มีสภาพคล่องน้อยกว่า premium (ส่วนต่างระหว่าง futures และ spot) ผันผวนมากกว่า ทำให้ funding แกว่งในช่วงกว้างกว่า

- ความถี่การจ่าย กระดานส่วนใหญ่จ่าย funding ทุก 8 ชั่วโมง (00:00, 08:00, 16:00 UTC) แต่บางกระดาน (Bybit สำหรับบางคู่, dYdX) จ่ายทุกชั่วโมง ซึ่งสร้างโอกาสเพิ่มเติม

ความแตกต่างที่เกิดขึ้นทั่วไป

ในตลาดที่สงบ funding rate บนกระดานหลักจะใกล้เคียงกัน โดยต่างกันเพียง 0.001-0.005% แต่ช่วงที่มีความผันผวนสูง ความแตกต่างจะขยายใหญ่ขึ้น:

| ช่วงตลาด | Binance | Bybit | OKX | dYdX | Spread |

|---|---|---|---|---|---|

| สงบ | 0.01% | 0.012% | 0.009% | 0.01% | ~0.003% |

| แนวโน้มขึ้น | 0.03% | 0.05% | 0.025% | 0.04% | ~0.025% |

| ขึ้นรุนแรง | 0.1% | 0.2% | 0.08% | 0.15% | ~0.12% |

| แนวโน้มลง | -0.02% | -0.01% | -0.025% | -0.015% | ~0.015% |

Spread 0.025% ต่อ 8 ชั่วโมง คือ 0.075% ต่อวัน ด้วยขนาด position 75/วัน หรือ ~$2,250/เดือน โดยไม่มีความเสี่ยงด้านทิศทาง

กลไกพื้นฐานของอาร์บิทราจ

ไอเดียเรียบง่าย: เปิด position ตรงข้ามบนสองกระดาน เพื่อรับ funding จากกระดานหนึ่งและจ่ายน้อยกว่าบนอีกกระดาน

ตัวอย่าง

Binance: funding rate = +0.01% (long จ่ายให้ short) Bybit: funding rate = +0.04% (long จ่ายให้ short)

การดำเนินการ:

- เปิด short บน Bybit — รับ 0.04% ทุก 8 ชั่วโมง

- เปิด long บน Binance — จ่าย 0.01% ทุก 8 ชั่วโมง

- Position สะท้อนกัน — ความเสี่ยงด้านราคาเป็นกลาง

- กำไรสุทธิ: 0.04% - 0.01% = 0.03% ต่อ 8 ชั่วโมง

ต่อวัน (3 ครั้ง): 0.09% ต่อเดือน: ~2.7% โดยไม่มีความเสี่ยงด้านทิศทาง

def funding_arbitrage_pnl(

rate_short_exchange: float, # rate on the exchange where we short

rate_long_exchange: float, # rate on the exchange where we long

position_size: float, # position size in USD

payments_per_day: int = 3,

days: int = 30,

) -> float:

"""

PnL from funding rate arbitrage over a period.

With positive funding: short receives, long pays.

With negative funding: short pays, long receives.

"""

spread = rate_short_exchange - rate_long_exchange

daily_pnl = spread * payments_per_day * position_size

return daily_pnl * days

pnl = funding_arbitrage_pnl(0.0004, 0.0001, 100_000, days=30)

ความเสี่ยงและกับดัก

กลยุทธ์นี้ดูเหมือน "เงินฟรี" แต่ไม่ใช่ มีความเสี่ยงที่ร้ายแรงหลายประการ

1. ราคาแตกต่างกันระหว่างกระดาน

Position บนกระดานต่างกันไม่ได้อยู่ที่ราคาเดียวกัน Spread ระหว่าง Binance และ Bybit ปกติอยู่ที่ 0.01-0.05% แต่ช่วงที่ความผันผวนสูงอาจถึง 0.5-1% ถ้าคุณไม่เปิด position พร้อมกัน ความแตกต่างอาจกินกำไรจาก funding หมด

วิธีแก้: เปิดพร้อมกันผ่าน API ด้วย latency น้อยที่สุด อุดมคติคือ server collocated ใกล้กับทั้งสองกระดาน

2. Funding Rate เปลี่ยนแปลง

คุณเปิด position ที่ spread 0.03% หนึ่งชั่วโมงต่อมา spread แคบลงเหลือ 0.005% หรือพลิกกลับ ตอนนี้คุณจ่ายบนทั้งสองกระดาน

วิธีแก้: ติดตาม spread แบบ real-time และปิดอัตโนมัติเมื่อ spread ลดลงต่ำกว่าเกณฑ์

def should_close(

current_spread: float,

entry_spread: float,

min_spread: float = 0.0001, # 0.01%

trading_costs: float = 0.0005, # 0.05% for opening + closing

) -> bool:

"""

Close the position if the spread has fallen below the threshold

or if the current spread does not cover trading costs.

"""

return current_spread < min_spread or current_spread < trading_costs

3. ค่าธรรมเนียมการซื้อขาย

การเปิดและปิด position บนสองกระดานหมายถึง 4 คำสั่ง ที่ค่าธรรมเนียม maker 0.02% และ taker 0.05%:

- สถานการณ์ดีที่สุด (ทั้งหมด maker):

- สถานการณ์แย่ที่สุด (ทั้งหมด taker):

เพื่อให้ค่าธรรมเนียมคุ้มทุน ต้องถือ position นานพอ:

def breakeven_days(

total_commissions_pct: float, # total commissions in %

spread: float, # funding rate spread

payments_per_day: int = 3,

) -> float:

daily_income = spread * payments_per_day

return total_commissions_pct / daily_income if daily_income > 0 else float('inf')

4. ข้อกำหนด Margin

Position บนทั้งสองกระดานต้องการหลักประกัน ที่ leverage 5x บนแต่ละกระดานด้วย position $100K:

- Binance: หลักประกัน $20K

- Bybit: หลักประกัน $20K

- รวมที่ถูกล็อค: **100K

ผลตอบแทนต่อทุน:

ที่ leverage 10x หลักประกันลดเหลือ $20K ROC เพิ่มขึ้นเป็น 13.5% แต่ความเสี่ยง liquidation จากความแตกต่างของราคาก็เพิ่มขึ้นด้วย

5. ความเสี่ยง Liquidation

ถ้าราคาของสินทรัพย์เคลื่อนที่อย่างรวดเร็ว หนึ่งใน position จะมีขาดทุนที่ยังไม่รับรู้ บนกระดานที่ position ขาดทุน ต้องรักษา margin ไว้ ถ้า margin ไม่เพียงพอจะถูก liquidation ในขณะที่กำไรบนกระดานอื่นไม่ช่วยได้ — มันอยู่ในบัญชีอื่น

วิธีแก้:

- รักษาสำรอง margin ไว้ (อย่างน้อย 2x ขั้นต่ำ)

- ตั้งการแจ้งเตือนระดับ margin

- Rebalancing อัตโนมัติ: เมื่อเกิดความไม่สมดุล — โอนเงินระหว่างกระดาน

ระบบติดตาม Funding Rate

ก้าวแรกสู่อาร์บิทราจคือการรวบรวมข้อมูล คุณต้องติดตาม funding rate บนทุกกระดานที่สนใจแบบ real-time

import asyncio

import ccxt.pro as ccxt

from dataclasses import dataclass

from datetime import datetime

@dataclass

class FundingSnapshot:

exchange: str

symbol: str

rate: float

next_funding_time: datetime

timestamp: datetime

class FundingMonitor:

"""

Monitor funding rates across multiple exchanges.

"""

def __init__(self, symbols: list[str], exchanges: list[str]):

self.symbols = symbols

self.exchanges = {

name: getattr(ccxt, name)() for name in exchanges

}

self.latest: dict[str, dict[str, FundingSnapshot]] = {}

async def fetch_funding(self, exchange_name: str, exchange, symbol: str):

"""Fetch current funding rate from an exchange."""

try:

funding = await exchange.fetch_funding_rate(symbol)

return FundingSnapshot(

exchange=exchange_name,

symbol=symbol,

rate=funding['fundingRate'],

next_funding_time=datetime.fromtimestamp(

funding['fundingTimestamp'] / 1000

),

timestamp=datetime.utcnow(),

)

except Exception as e:

print(f"Error fetching {exchange_name} {symbol}: {e}")

return None

async def scan(self) -> list[dict]:

"""

Scan all exchanges and find arbitrage opportunities.

"""

tasks = []

for ex_name, ex in self.exchanges.items():

for symbol in self.symbols:

tasks.append(self.fetch_funding(ex_name, ex, symbol))

snapshots = await asyncio.gather(*tasks)

snapshots = [s for s in snapshots if s is not None]

by_symbol: dict[str, list[FundingSnapshot]] = {}

for s in snapshots:

by_symbol.setdefault(s.symbol, []).append(s)

opportunities = []

for symbol, rates in by_symbol.items():

rates.sort(key=lambda x: x.rate)

lowest = rates[0] # long here (pay less)

highest = rates[-1] # short here (receive more)

spread = highest.rate - lowest.rate

opportunities.append({

'symbol': symbol,

'long_exchange': lowest.exchange,

'long_rate': lowest.rate,

'short_exchange': highest.exchange,

'short_rate': highest.rate,

'spread': spread,

'annualized': spread * 3 * 365 * 100, # in % annualized

})

return sorted(opportunities, key=lambda x: -x['spread'])

ตัวอย่างผลลัพธ์

Symbol | Long @ | Rate | Short @ | Rate | Spread | APR

-----------+-------------+---------+-------------+---------+---------+--------

ETHUSDT | Binance | 0.010% | Bybit | 0.040% | 0.030% | 32.9%

BTCUSDT | OKX | 0.008% | Binance | 0.020% | 0.012% | 13.1%

SOLUSDT | Binance | 0.015% | dYdX | 0.055% | 0.040% | 43.8%

ARBUSDT | Bybit | 0.005% | OKX | 0.030% | 0.025% | 27.4%

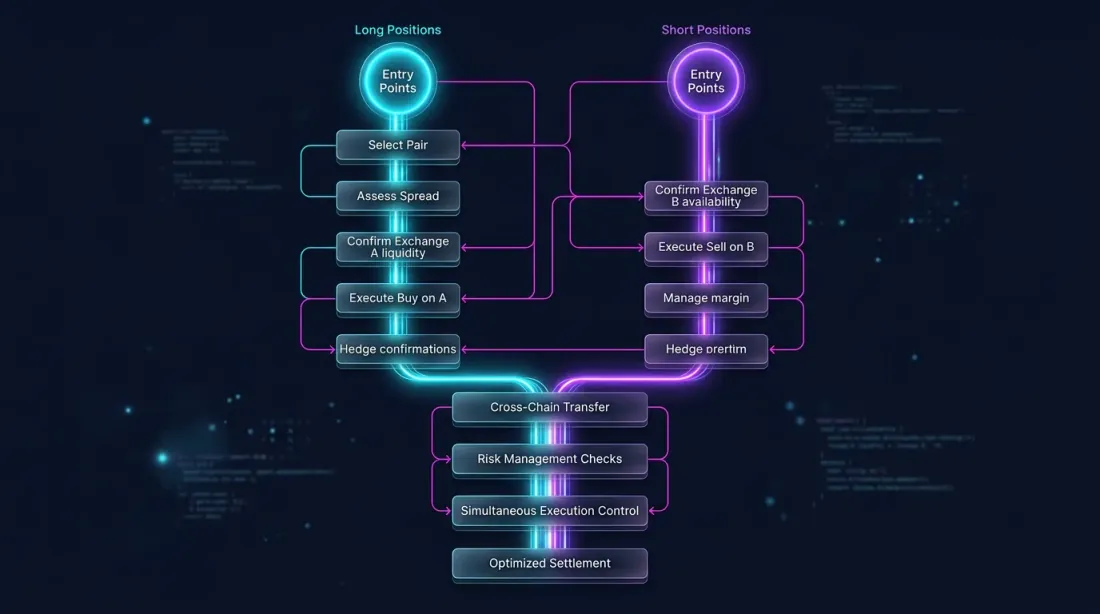

การดำเนินการ: เปิด Position พร้อมกัน

สิ่งสำคัญอย่างยิ่งคือต้องเปิด long และ short พร้อมกันให้ได้มากที่สุด เพื่อหลีกเลี่ยงการรับความเสี่ยงด้านทิศทาง

import asyncio

async def execute_arbitrage(

long_exchange,

short_exchange,

symbol: str,

size: float,

max_slippage_pct: float = 0.05,

):

"""

Simultaneously open a long and short on two exchanges.

"""

long_ticker = await long_exchange.fetch_ticker(symbol)

short_ticker = await short_exchange.fetch_ticker(symbol)

price_spread = abs(

long_ticker['ask'] - short_ticker['bid']

) / long_ticker['ask'] * 100

if price_spread > max_slippage_pct:

raise ValueError(

f"Price spread {price_spread:.3f}% exceeds max slippage"

)

long_order, short_order = await asyncio.gather(

long_exchange.create_market_buy_order(symbol, size),

short_exchange.create_market_sell_order(symbol, size),

)

return long_order, short_order

การจัดการ Position

หลังจากเปิดแล้ว ต้องติดตามอย่างต่อเนื่อง:

- Funding rate spread ถ้า spread แคบลงต่ำกว่าเกณฑ์ — ปิด

- ยอด Margin ถ้า margin บนกระดานใดกระดานหนึ่งลดลงต่ำกว่าระดับปลอดภัย — rebalance หรือปิด

- ความแตกต่างของราคา ถ้า unrealized P&L ด้านใดด้านหนึ่งเกินขีดจำกัด — ปิด

async def monitor_and_manage(

long_exchange,

short_exchange,

symbol: str,

size: float,

min_spread: float = 0.0001,

max_unrealized_loss_pct: float = 2.0,

check_interval: int = 60,

):

"""

Monitor an open arbitrage position.

"""

while True:

long_funding = await long_exchange.fetch_funding_rate(symbol)

short_funding = await short_exchange.fetch_funding_rate(symbol)

current_spread = (

short_funding['fundingRate'] - long_funding['fundingRate']

)

long_balance = await long_exchange.fetch_balance()

short_balance = await short_exchange.fetch_balance()

long_positions = await long_exchange.fetch_positions([symbol])

short_positions = await short_exchange.fetch_positions([symbol])

long_upnl = long_positions[0]['unrealizedPnl'] if long_positions else 0

short_upnl = short_positions[0]['unrealizedPnl'] if short_positions else 0

total_upnl_pct = (long_upnl + short_upnl) / size * 100

if current_spread < min_spread:

print(f"Spread collapsed: {current_spread:.4%}")

await close_both(long_exchange, short_exchange, symbol, size)

break

if abs(total_upnl_pct) > max_unrealized_loss_pct:

print(f"Unrealized loss exceeded: {total_upnl_pct:.2f}%")

await close_both(long_exchange, short_exchange, symbol, size)

break

await asyncio.sleep(check_interval)

รูปแบบขั้นสูง

อาร์บิทราจ Spot-Perp

แทนที่จะใช้ futures บนสองกระดาน คุณสามารถใช้ spot + futures บนกระดานเดียวกัน:

- ซื้อ spot (ไม่มี funding)

- Short perpetual futures (รับ funding เมื่ออัตราเป็นบวก)

ข้อดี: ทุกอย่างอยู่บนกระดานเดียว จัดการ margin ง่ายกว่า ข้อเสีย: ใช้ได้เฉพาะเมื่อ funding เป็นบวก (long จ่ายให้ short) ซึ่งเกิดขึ้น ~70% ของเวลาในตลาดขาขึ้น

def spot_perp_carry(

funding_rate: float, # current funding rate

spot_fee: float = 0.001, # spot commission (0.1%)

perp_fee: float = 0.0005, # futures commission (0.05%)

leverage: int = 1,

) -> dict:

"""

Calculate the yield of a spot-perp carry trade.

"""

total_fees = (spot_fee + perp_fee) * 2 # opening + closing

daily_income = funding_rate * 3

breakeven_days = total_fees / daily_income if daily_income > 0 else float('inf')

return {

'daily_income_pct': daily_income * 100,

'monthly_income_pct': daily_income * 30 * 100,

'annualized_pct': daily_income * 365 * 100,

'total_fees_pct': total_fees * 100,

'breakeven_days': breakeven_days,

}

result = spot_perp_carry(0.0003)

อาร์บิทราจหลายกระดาน

เมื่อติดตาม 5+ กระดานพร้อมกัน คุณสามารถหาโอกาสที่ดีกว่าได้ อัลกอริทึม:

- รวบรวม funding rate จากทุกกระดาน

- หาคู่ที่มี spread สูงสุด

- ตรวจสอบสภาพคล่องและความลึกของ order book บนทั้งสองกระดาน

- ถ้า spread > เกณฑ์ — เปิด position

- Rescan อย่างต่อเนื่อง: ถ้าคู่ที่ดีที่สุดเปลี่ยน — หมุนเวียน

def find_best_pair(

rates: dict[str, float], # {"binance": 0.01, "bybit": 0.04, "okx": 0.02}

min_spread: float = 0.0002,

) -> tuple[str, str, float] | None:

"""

Find the exchange pair with the maximum funding rate spread.

Returns: (long_exchange, short_exchange, spread) or None.

"""

exchanges = list(rates.keys())

best = None

for i, ex_long in enumerate(exchanges):

for ex_short in exchanges[i+1:]:

if rates[ex_long] < rates[ex_short]:

spread = rates[ex_short] - rates[ex_long]

long_ex, short_ex = ex_long, ex_short

else:

spread = rates[ex_long] - rates[ex_short]

long_ex, short_ex = ex_short, ex_long

if spread >= min_spread:

if best is None or spread > best[2]:

best = (long_ex, short_ex, spread)

return best

การทำนาย Funding Rate

Funding rate คำนวณด้วยสูตรที่รวม premium index — ส่วนต่างระหว่างราคา futures และ spot Premium อัปเดตบ่อยกว่า funding (ทุกนาที vs ทุก 8 ชั่วโมง) นั่นหมายความว่าคุณสามารถ ทำนาย funding rate ครั้งถัดไปได้ก่อนการจ่ายเงินเป็นนาทีหรือหลายชั่วโมง

def predict_next_funding(

premium_index: float,

interest_rate: float = 0.0001, # 0.01% per 8h (standard)

clamp_range: float = 0.0005, # ±0.05%

) -> float:

"""

Predict the next funding rate based on the current premium index.

Binance formula: FR = clamp(Premium - Interest, -0.05%, 0.05%) + Interest

"""

diff = premium_index - interest_rate

clamped = max(-clamp_range, min(clamp_range, diff))

return clamped + interest_rate

เมื่อรู้ funding rate ที่คาดการณ์ได้ คุณสามารถเปิด position ก่อน การจ่าย เมื่อ spread ยังไม่ดึงดูดความสนใจของ arbitrageurs รายอื่น

ข้อกำหนดด้านโครงสร้างพื้นฐาน

สำหรับอาร์บิทราจ Funding Rate อย่างจริงจัง คุณต้องการโครงสร้างพื้นฐาน:

| ส่วนประกอบ | ขั้นต่ำ | เหมาะสมที่สุด |

|---|---|---|

| เซิร์ฟเวอร์ | Cloud VPS | Collocated ใกล้กระดาน |

| Latency | < 500ms | < 50ms |

| API keys | 2 กระดาน | 5+ กระดาน |

| ทุนต่อกระดาน | $10K ต่อกระดาน | $50K+ ต่อกระดาน |

| การติดตาม | Logs + alerts | Dashboard + auto-rebalancing |

| ข้อมูล | REST API polling | WebSocket streaming |

เศรษฐศาสตร์ที่มาตราส่วนต่างกัน

| ทุน | Position (5x) | Spread 0.03% | PnL รายเดือน | ROC |

|---|---|---|---|---|

| $10K | $25K | 0.03% | ~$675 | ~6.75% |

| $50K | $125K | 0.03% | ~$3,375 | ~6.75% |

| $200K | $500K | 0.03% | ~$13,500 | ~6.75% |

ROC ไม่ขึ้นอยู่กับมาตราส่วน (เมื่อสภาพคล่องเพียงพอ) แต่กำไรสัมบูรณ์ที่ทุน $10K อาจไม่คุ้มกับต้นทุนโครงสร้างพื้นฐานและเวลาที่ใช้

บทสรุป

อาร์บิทราจ Funding Rate เป็นกลยุทธ์เชิงโครงสร้างที่ delta-neutral ไม่ต้องการการทำนายราคา แต่ต้องการ:

- โครงสร้างพื้นฐาน — ติดตาม rate แบบ real-time บนหลายกระดาน

- ความเร็วในการดำเนินการ — เปิด position พร้อมกันบนกระดานต่างๆ

- การจัดการความเสี่ยง — ควบคุม margin ความแตกต่างของราคา และการเปลี่ยนแปลง spread

- ทุน — กำไรเป็นสัดส่วนกับขนาด position

Funding rate spread ไม่คงที่ จะขยายตัวในช่วงที่มีความผันผวนและแคบลงในช่วงที่สงบ งานคือการหาและใช้ประโยชน์จากความแตกต่างโดยอัตโนมัติในขณะที่มันยังคงอยู่

สำหรับข้อมูลเพิ่มเติมเกี่ยวกับวิธีที่ funding rate ส่งผลต่อกลยุทธ์ leverage — ดูบทความ Funding Rates Kill Your Leverage: Why PnL×50x Is a Fiction.

ลิงก์ที่เป็นประโยชน์

- Binance — Funding Rate History

- Binance — Introduction to Funding Rates

- Bybit — Understanding Funding Rates

- dYdX — Perpetual Funding Rate Mechanism

- Coinglass — Funding Rate Monitor

อ้างอิง

@article{soloviov2026fundingarbitrage,

author = {Soloviov, Eugen},

title = {Funding Rate Arbitrage Across Exchanges: How to Profit from Rate Differences},

year = {2026},

url = {https://marketmaker.cc/th/blog/post/funding-rate-arbitrage-cross-exchange},

description = {How funding rate arbitrage works across crypto exchanges, why rates differ on Binance, Bybit, OKX and dYdX, and how to build a monitoring and execution system.}

}

ผู้เขียน

Trading-systems engineer

Trading-systems engineer building bots since 2017: cross-exchange arbitrage (connected up to 30 venues), cointegration-based pairs arbitrage across spot and futures, scalping, news and sentiment-driven strategies, trend algorithms, and portfolio management and balancing algorithms. Also builds sub-millisecond order execution, big-data warehouses, backtesting engines, AI agents, and trading interfaces (incl. open-source profitmaker.cc). Stack: JS/TS, Python, Rust/Zig/Go, DevOps, backend, frontend, architecture.

อ่านเพิ่มเติม

Funding Rate ทำลาย Leverage ของคุณ: ทำไม PnL×50x ถึงเป็นแค่ภาพลวงตา

Statistical Arbitrage และ Pairs Trading ในตลาด Crypto: จาก Cointegration สู่ Kalman Filter