نهج المسافة في تداول الأزواج: التنفيذ والتحليل باستخدام Rust

اكتسب نهج المسافة في تداول الأزواج شعبية كبيرة بفضل بساطته الأنيقة وفعاليته. تحدد هذه التقنية أزواج الأصول من خلال مقاييس إحصائية وتتداول بناءً على تباعد وتقارب علاقات أسعارها. يقدم هذا المقال تحليلاً شاملاً لمنهجيات نهج المسافة الأساسية والمتقدمة، مع تطبيقات عملية بلغة Rust مصممة للمتداولين عاليي التردد، ومطوري الخوارزميات، والرياضيين، والمبرمجين الباحثين عن حلول متينة.

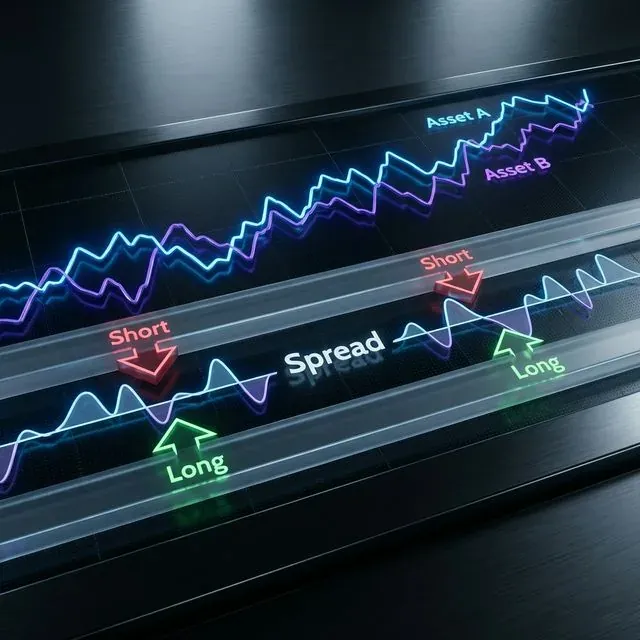

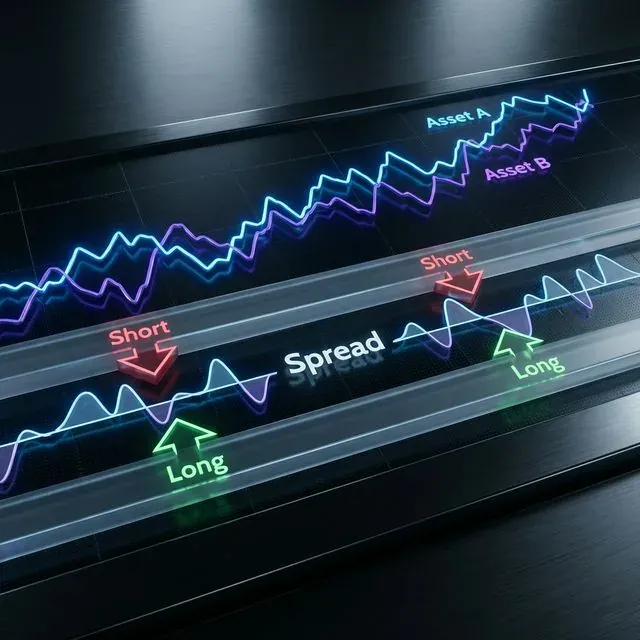

تصور نهج المسافة: الأصلان A وB يتتبعان بعضهما البعض، مع توليد إشارات التداول بناءً على تباعد الفارق (Long/Short)

تصور نهج المسافة: الأصلان A وB يتتبعان بعضهما البعض، مع توليد إشارات التداول بناءً على تباعد الفارق (Long/Short)

الأساس النظري لنهج المسافة

يُنشئ نهج المسافة إطاراً لتداول الأزواج يعتمد على حركات الأسعار المُطبّعة بين الأصول. في جوهره، يستخدم قياسات المسافة الإقليدية المربعة لتحديد الأصول التي تتحرك تاريخياً معاً، ويولّد إشارات تداول عندما يتجاوز تباعد أسعارها المُطبّعة عتبات ذات دلالة إحصائية[2].

يتكون هذا النهج من مرحلتين رئيسيتين:

- تشكيل الأزواج - تحديد أزواج الأصول المرتبطة إحصائياً

- توليد إشارات التداول - إنشاء قواعد الدخول والخروج بناءً على التباعد

الأساس الرياضي

يستخدم التطبيق الأساسي المسافة الإقليدية بين سلاسل الأسعار المُطبّعة. لأصلين بسلسلتي أسعار مُطبّعتين X وY، نحسب:

fn euclidean_squared_distance(x: &[f64], y: &[f64]) -> f64 {

assert_eq!(x.len(), y.len(), "Time series must have equal length");

x.iter()

.zip(y.iter())

.map(|(xi, yi)| (xi - yi).powi(2))

.sum()

}

يساعد مقياس المسافة هذا في تحديد الأصول التي تتحرك تاريخياً معاً، مما يوفر الأساس لفرص المراجحة الإحصائية[2].

تنفيذ نهج المسافة الأساسي

تطبيع البيانات

قبل حساب المسافات، يجب تطبيع بيانات الأسعار لإنشاء مقاييس قابلة للمقارنة. يُطبّق تطبيع Min-Max عادةً:

fn min_max_normalize(prices: &[f64]) -> Vec<f64> {

if prices.is_empty() {

return Vec::new();

}

let min_price = prices.iter().fold(f64::INFINITY, |a, &b| a.min(b));

let max_price = prices.iter().fold(f64::NEG_INFINITY, |a, &b| a.max(b));

let range = max_price - min_price;

if range.abs() < f64::EPSILON {

return vec![0.5; prices.len()];

}

prices.iter()

.map(|&price| (price - min_price) / range)

.collect()

}

البحث عن أقرب الأزواج

نحدد الأزواج المحتملة بحساب المسافة الإقليدية بين جميع تركيبات الأصول واختيار تلك ذات أصغر المسافات:

#[derive(Debug, Clone)]

struct StockPair {

stock1_idx: usize,

stock2_idx: usize,

distance: f64,

}

impl PartialEq for StockPair {

fn eq(&self, other: &Self) -> bool {

self.distance.eq(&other.distance)

}

}

impl Eq for StockPair {}

impl PartialOrd for StockPair {

fn partial_cmp(&self, other: &Self) -> Option<std::cmp::Ordering> {

self.distance.partial_cmp(&other.distance)

}

}

impl Ord for StockPair {

fn cmp(&self, other: &Self) -> std::cmp::Ordering {

self.partial_cmp(other).unwrap_or(std::cmp::Ordering::Equal)

}

}

fn find_closest_pairs(normalized_prices: &[Vec<f64>], top_n: usize) -> Vec<StockPair> {

let stock_count = normalized_prices.len();

let mut pairs = BinaryHeap::new();

for i in 0..stock_count {

for j in (i+1)..stock_count {

let distance = euclidean_squared_distance(&normalized_prices[i], &normalized_prices[j]);

pairs.push(Reverse(StockPair {

stock1_idx: i,

stock2_idx: j,

distance,

}));

// Keep only top N pairs

if pairs.len() > top_n {

pairs.pop();

}

}

}

// Convert from heap to vector and reverse to get ascending order

pairs.into_iter().map(|Reverse(pair)| pair).collect()

}

حساب التقلب التاريخي

حساب التقلب التاريخي ضروري لتحديد عتبات تداول مناسبة:

fn calculate_spread_volatility(normalized_price1: &[f64], normalized_price2: &[f64]) -> f64 {

assert_eq!(normalized_price1.len(), normalized_price2.len());

// Calculate price spread

let spread: Vec<f64> = normalized_price1.iter()

.zip(normalized_price2.iter())

.map(|(p1, p2)| p1 - p2)

.collect();

// Calculate mean of spread

let mean = spread.iter().sum::<f64>() / spread.len() as f64;

// Calculate standard deviation

let variance = spread.iter()

.map(|&x| (x - mean).powi(2))

.sum::<f64>() / spread.len() as f64;

variance.sqrt()

}

أساليب الاختيار المتقدمة

تصفية مجموعات الصناعة

تقييد اختيار الأزواج على نفس الصناعة يمكن أن يحسّن الأداء باختيار أصول مرتبطة اقتصادياً:

fn find_industry_pairs(

normalized_prices: &[Vec<f64>],

industry_codes: &[usize],

top_n_per_industry: usize

) -> Vec<StockPair> {

// Group stocks by industry

let mut industry_groups: std::collections::HashMap<usize, Vec<usize>> = std::collections::HashMap::new();

for (idx, &code) in industry_codes.iter().enumerate() {

industry_groups.entry(code).or_default().push(idx);

}

// Find closest pairs within each industry

let mut all_pairs = Vec::new();

for (_industry_code, stock_indices) in industry_groups {

let mut industry_pairs = Vec::new();

for i in 0..stock_indices.len() {

for j in (i+1)..stock_indices.len() {

let stock1_idx = stock_indices[i];

let stock2_idx = stock_indices[j];

let distance = euclidean_squared_distance(

&normalized_prices[stock1_idx],

&normalized_prices[stock2_idx]

);

industry_pairs.push(StockPair {

stock1_idx,

stock2_idx,

distance,

});

}

}

// Sort pairs by distance

industry_pairs.sort_by(|a, b| a.distance.partial_cmp(&b.distance).unwrap());

// Take top N from each industry

let top_pairs: Vec<StockPair> = industry_pairs.into_iter()

.take(top_n_per_industry)

.collect();

all_pairs.extend(top_pairs);

}

all_pairs

}

نهج التقاطعات الصفرية يحدد الأزواج ذات التقارب والتباعد المتكرر، مما قد يشير إلى فرص تداول أكثر ربحية:

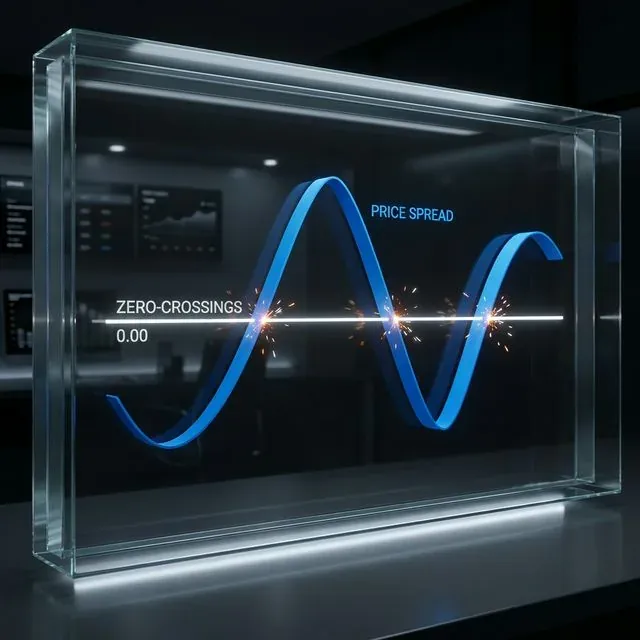

مفهوم التقاطعات الصفرية: تحديد الأزواج التي تعود للمتوسط بشكل متكرر، يُشار إليها بتقاطع الفارق مع خط الصفر

مفهوم التقاطعات الصفرية: تحديد الأزواج التي تعود للمتوسط بشكل متكرر، يُشار إليها بتقاطع الفارق مع خط الصفر

fn count_zero_crossings(spread: &[f64]) -> usize {

if spread.len() < 2 {

return 0;

}

let mut count = 0;

for i in 1..spread.len() {

if (spread[i-1] < 0.0 && spread[i] >= 0.0) ||

(spread[i-1] >= 0.0 && spread[i] < 0.0) {

count += 1;

}

}

count

}

fn find_zero_crossing_pairs(

normalized_prices: &[Vec<f64>],

top_distance_threshold: f64,

min_crossings: usize

) -> Vec<StockPair> {

let stock_count = normalized_prices.len();

let mut qualifying_pairs = Vec::new();

for i in 0..stock_count {

for j in (i+1)..stock_count {

let distance = euclidean_squared_distance(&normalized_prices[i], &normalized_prices[j]);

// Only consider pairs with distance below threshold

if distance < top_distance_threshold {

// Calculate spread

let spread: Vec<f64> = normalized_prices[i].iter()

.zip(normalized_prices[j].iter())

.map(|(p1, p2)| p1 - p2)

.collect();

let crossings = count_zero_crossings(&spread);

if crossings >= min_crossings {

qualifying_pairs.push(StockPair {

stock1_idx: i,

stock2_idx: j,

distance,

});

}

}

}

}

// Sort by number of crossings (could extend StockPair to include this)

qualifying_pairs.sort_by(|a, b| a.distance.partial_cmp(&b.distance).unwrap());

qualifying_pairs

}

اعتبار الانحراف المعياري التاريخي

يعالج هذا الأسلوب قيداً في النهج الأساسي بإعطاء الأولوية للأزواج ذات تقلب الفارق الأعلى، مما يمكن أن يزيد إمكانية الربح:

fn find_highsd_pairs(

normalized_prices: &[Vec<f64>],

top_distance_count: usize,

min_volatility: f64

) -> Vec<StockPair> {

let stock_count = normalized_prices.len();

let mut all_pairs = Vec::new();

for i in 0..stock_count {

for j in (i+1)..stock_count {

let distance = euclidean_squared_distance(&normalized_prices[i], &normalized_prices[j]);

// Calculate spread volatility

let spread: Vec<f64> = normalized_prices[i].iter()

.zip(normalized_prices[j].iter())

.map(|(p1, p2)| p1 - p2)

.collect();

let volatility = calculate_spread_volatility(&normalized_prices[i], &normalized_prices[j]);

if volatility >= min_volatility {

all_pairs.push(StockPair {

stock1_idx: i,

stock2_idx: j,

distance,

});

}

}

}

// Sort by distance

all_pairs.sort_by(|a, b| a.distance.partial_cmp(&b.distance).unwrap());

// Take top N pairs with highest volatility that meet distance criteria

all_pairs.into_iter().take(top_distance_count).collect()

}

النهج المتقدم: طريقة ارتباط بيرسون

يقدم نهج ارتباط بيرسون عدة مزايا مقارنة بنهج المسافة الأساسي، حيث يركز على ارتباطات العوائد بدلاً من مسافات الأسعار[1].

التنفيذ بلغة Rust

fn pearson_correlation(x: &[f64], y: &[f64]) -> f64 {

assert_eq!(x.len(), y.len(), "Arrays must have the same length");

let n = x.len() as f64;

let sum_x: f64 = x.iter().sum();

let sum_y: f64 = y.iter().sum();

let sum_xx: f64 = x.iter().map(|&val| val * val).sum();

let sum_yy: f64 = y.iter().map(|&val| val * val).sum();

let sum_xy: f64 = x.iter().zip(y.iter()).map(|(&xi, &yi)| xi * yi).sum();

let numerator = n * sum_xy - sum_x * sum_y;

let denominator = ((n * sum_xx - sum_x * sum_x) * (n * sum_yy - sum_y * sum_y)).sqrt();

if denominator.abs() < f64::EPSILON {

return 0.0;

}

numerator / denominator

}

struct PearsonPair {

stock_idx: usize,

comover_indices: Vec<usize>,

correlations: Vec<f64>,

}

fn find_pearson_pairs(returns: &[Vec<f64>], top_n_comovers: usize) -> Vec<PearsonPair> {

let stock_count = returns.len();

let mut all_pairs = Vec::new();

for i in 0..stock_count {

let mut correlations = Vec::with_capacity(stock_count - 1);

for j in 0..stock_count {

if i == j {

continue;

}

let correlation = pearson_correlation(&returns[i], &returns[j]).abs();

correlations.push((j, correlation));

}

// Sort by correlation (highest first)

correlations.sort_by(|a, b| b.1.partial_cmp(&a.1).unwrap_or(std::cmp::Ordering::Equal));

// Take top N comovers

let top_comovers: Vec<(usize, f64)> = correlations.into_iter()

.take(top_n_comovers)

.collect();

let (comover_indices, correlation_values): (Vec<usize>, Vec<f64>) =

top_comovers.into_iter().unzip();

all_pairs.push(PearsonPair {

stock_idx: i,

comover_indices,

correlations: correlation_values,

});

}

all_pairs

}

تشكيل المحفظة وحساب بيتا

ينشئ نهج بيرسون محافظ من الأصول المتحركة معاً لكل سهم، ثم يحسب معاملات الانحدار:

fn calculate_beta(stock_returns: &[f64], portfolio_returns: &[f64]) -> f64 {

let cov_xy = covariance(stock_returns, portfolio_returns);

let var_x = variance(portfolio_returns);

if var_x.abs() < f64::EPSILON {

return 0.0;

}

cov_xy / var_x

}

fn covariance(x: &[f64], y: &[f64]) -> f64 {

assert_eq!(x.len(), y.len());

let n = x.len() as f64;

let mean_x: f64 = x.iter().sum::<f64>() / n;

let mean_y: f64 = y.iter().sum::<f64>() / n;

let sum_cov: f64 = x.iter()

.zip(y.iter())

.map(|(&xi, &yi)| (xi - mean_x) * (yi - mean_y))

.sum();

sum_cov / n

}

fn variance(x: &[f64]) -> f64 {

let n = x.len() as f64;

let mean: f64 = x.iter().sum::<f64>() / n;

let sum_var: f64 = x.iter()

.map(|&xi| (xi - mean).powi(2))

.sum();

sum_var / n

}

توليد إشارات التداول

الخطوة الأخيرة في كلا النهجين هي توليد إشارات التداول بناءً على عتبات التباعد:

enum TradingSignal {

Long,

Short,

Neutral

}

struct TradePosition {

stock1_idx: usize,

stock2_idx: usize,

signal: TradingSignal,

entry_spread: f64,

timestamp: usize,

}

fn generate_trading_signals(

normalized_prices: &[Vec<f64>],

pairs: &[StockPair],

threshold_multiplier: f64,

volatilities: &[f64],

current_time: usize

) -> Vec<TradePosition> {

let mut positions = Vec::new();

for (pair_idx, pair) in pairs.iter().enumerate() {

let stock1_idx = pair.stock1_idx;

let stock2_idx = pair.stock2_idx;

// Calculate current spread

let current_spread = normalized_prices[stock1_idx][current_time] -

normalized_prices[stock2_idx][current_time];

let threshold = threshold_multiplier * volatilities[pair_idx];

let signal = if current_spread > threshold {

// Stock1 is overvalued relative to Stock2

TradingSignal::Short

} else if current_spread < -threshold {

// Stock1 is undervalued relative to Stock2

TradingSignal::Long

} else {

TradingSignal::Neutral

};

if signal != TradingSignal::Neutral {

positions.push(TradePosition {

stock1_idx,

stock2_idx,

signal,

entry_spread: current_spread,

timestamp: current_time,

});

}

}

positions

}

تحسين الأداء

في أنظمة التداول عالية التردد، الأداء حاسم. يمكن لتعليمات SIMD (تعليمة واحدة، بيانات متعددة) تسريع حسابات المسافة بشكل كبير:

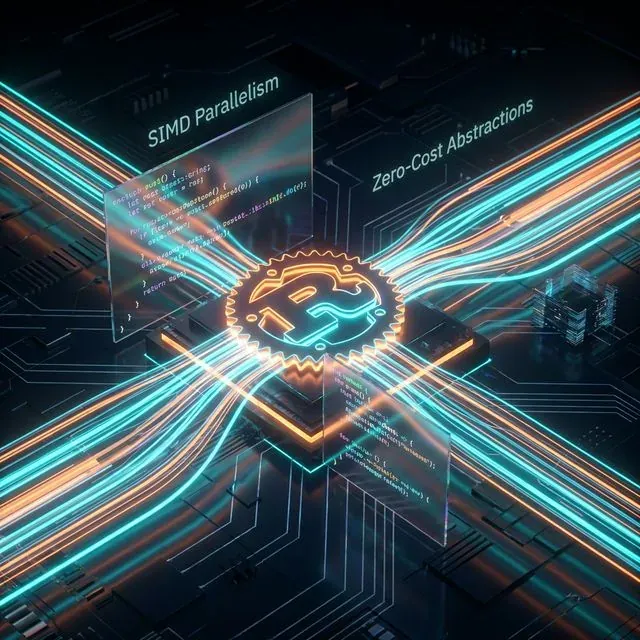

تسريع SIMD: استخدام التوازي على مستوى البيانات في Rust لمعالجة نقاط أسعار متعددة في وقت واحد، مما يقلل زمن الاستجابة بشكل جذري

تسريع SIMD: استخدام التوازي على مستوى البيانات في Rust لمعالجة نقاط أسعار متعددة في وقت واحد، مما يقلل زمن الاستجابة بشكل جذري

#[cfg(target_arch = "x86_64")]

use std::arch::x86_64::*;

#[cfg(target_arch = "x86_64")]

#[inline]

unsafe fn euclidean_distance_simd(x: &[f32], y: &[f32]) -> f32 {

assert_eq!(x.len(), y.len());

let mut sum = _mm256_setzero_ps();

let chunks = x.len() / 8;

for i in 0..chunks {

let xi = _mm256_loadu_ps(&x[i * 8]);

let yi = _mm256_loadu_ps(&y[i * 8]);

let diff = _mm256_sub_ps(xi, yi);

let squared = _mm256_mul_ps(diff, diff);

sum = _mm256_add_ps(sum, squared);

}

// Handle the remaining elements

let mut result = _mm256_reduce_add_ps(sum);

for i in (chunks * 8)..x.len() {

result += (x[i] - y[i]).powi(2);

}

result.sqrt()

}

// Helper function to sum SIMD vector

#[cfg(target_arch = "x86_64")]

#[inline(always)]

unsafe fn _mm256_reduce_add_ps(v: __m256) -> f32 {

let hilow = _mm256_extractf128_ps(v, 1);

let low = _mm256_castps256_ps128(v);

let sum128 = _mm_add_ps(hilow, low);

let hi64 = _mm_extractf128_si128(_mm_castps_si128(sum128), 1);

let low64 = _mm_castps_si128(sum128);

let sum64 = _mm_add_ps(_mm_castsi128_ps(hi64), _mm_castsi128_ps(low64));

_mm_cvtss_f32(_mm_hadd_ps(sum64, sum64))

}

يمكن للمعالجة غير المتزامنة تحسين الإنتاجية بشكل أكبر، خاصة عند التعامل مع أزواج أسهم متعددة:

use tokio::task;

use futures::future::join_all;

async fn process_pairs_async(

normalized_prices: &[Vec<f64>],

stock_count: usize,

chunk_size: usize

) -> Vec<StockPair> {

let mut tasks = Vec::new();

// Split work into chunks

let chunks = (stock_count + chunk_size - 1) / chunk_size;

for chunk in 0..chunks {

let start = chunk * chunk_size;

let end = std::cmp::min((chunk + 1) * chunk_size, stock_count);

let prices_clone = normalized_prices.to_vec();

let task = task::spawn(async move {

let mut pairs = Vec::new();

for i in start..end {

for j in (i+1)..stock_count {

let distance = euclidean_squared_distance(&prices_clone[i], &prices_clone[j]);

pairs.push(StockPair {

stock1_idx: i,

stock2_idx: j,

distance,

});

}

}

pairs

});

tasks.push(task);

}

// Await all tasks and combine results

let results = join_all(tasks).await;

let mut all_pairs = Vec::new();

for result in results {

if let Ok(pairs) = result {

all_pairs.extend(pairs);

}

}

// Sort by distance

all_pairs.sort_by(|a, b| a.distance.partial_cmp(&b.distance).unwrap_or(std::cmp::Ordering::Equal));

all_pairs

}

اختبار تنفيذ الاستراتيجية

لتقييم تنفيذنا، نحتاج إلى بنية اختبار مناسبة:

#[cfg(test)]

mod tests {

use super::*;

#[test]

fn test_normalization() {

let prices = vec![10.0, 15.0, 12.0, 18.0, 20.0];

let normalized = min_max_normalize(&prices);

let expected = vec![0.0, 0.5, 0.2, 0.8, 1.0];

for (a, b) in normalized.iter().zip(expected.iter()) {

assert!((a - b).abs() < 0.001);

}

}

#[test]

fn test_euclidean_distance() {

let x = vec![0.1, 0.2, 0.3, 0.4, 0.5];

let y = vec![0.15, 0.22, 0.35, 0.38, 0.53];

let distance = euclidean_squared_distance(&x, &y);

let expected = 0.0049; // Calculated manually

assert!((distance - expected).abs() < 0.0001);

}

#[test]

fn test_pearson_correlation() {

let x = vec![1.0, 2.0, 3.0, 4.0, 5.0];

let y = vec![5.0, 4.0, 3.0, 2.0, 1.0];

let corr = pearson_correlation(&x, &y);

let expected = -1.0; // Perfect negative correlation

assert!((corr - expected).abs() < 0.0001);

}

// Integration tests would be implemented in tests/ directory

}

بالنسبة لاختبارات التكامل، نتبع اتفاقية Rust بوضع الاختبارات في مجلد tests منفصل في جذر المشروع[15][18].

الخلاصة

يوفر نهج المسافة إطاراً متيناً لتداول الأزواج، حيث تقدم كل من المنهجيات الأساسية والمتقدمة فرصاً قيّمة للمراجحة الإحصائية. النهج الأساسي، بتركيزه على المسافة الإقليدية، يوفر البساطة والفعالية، بينما يوفر نهج ارتباط بيرسون مرونة إضافية وخصائص عودة تباعد أفضل محتملاً.

تجعل خصائص أداء Rust منها لغة مثالية لتنفيذ هذه الاستراتيجيات كثيفة الحسابات، خاصة مع تحسينات مثل SIMD والمعالجة المتزامنة. الجمع بين الدقة الإحصائية والتنفيذ الفعال يخلق مجموعة أدوات قوية للمتداولين الخوارزميين.

عند تنفيذ نظام تداول الأزواج، يجب مراعاة عدة اعتبارات:

- المفاضلة بين البساطة (النهج الأساسي) والقوة الإحصائية المعززة (نهج بيرسون)

- الموارد الحسابية المطلوبة لتحليل الأزواج على نطاق واسع

- تكاليف المعاملات، التي يمكن أن تؤثر بشكل كبير على الربحية[3]

- الحاجة إلى مراقبة مستمرة وإعادة معايرة الأزواج

من خلال الجمع بين نهج المسافة وقدرات أداء Rust، يمكن للمتداولين تطوير أنظمة مراجحة إحصائية عالية الكفاءة والفعالية قادرة على العمل بالسرعة والنطاق المطلوبين للأسواق الحديثة.

Citation

@software{soloviov2025distanceapproach,

author = {Soloviov, Eugen},

title = {Distance Approach in Pairs Trading: Implementation and Analysis with Rust},

year = {2025},

url = {https://marketmaker.cc/ar/blog/post/distance-approach-pairs-trading},

version = {0.1.0},

description = {A comprehensive analysis of basic and advanced Distance Approach methodologies for pairs trading, with practical implementations in Rust tailored for high-frequency traders and algorithmic developers.}

}

References

- Hudson Thames - Introduction to Distance Approach in Pairs Trading Part II

- Hudson Thames - Distance Approach in Pairs Trading Part I

- Reddit - Pairs Trading is Too Good to Be True?

- GitHub - Kucoin Arbitrage

- docs.rs - Euclidean Distance in geo crate

- Simple Linear Regression in Rust

- GitHub - correlation_rust

- docs.rs - Cointegration in algolotl-ta

- GitHub - trading_engine_rust

- docs.rs - distances crate

- Reddit - Looking for stats crate for Dickey-Fuller

- crates.io - crypto-pair-trader

- w3resource - Rust Structs and Enums Exercise

- Rust Book - Test Organization

- Design Patterns in Rust

- GitHub - simd-euclidean

- Rust by Example - Integration Testing

- YouTube - Integration Testing in Rust

- Stack Overflow - Calculate Total Distance Between Multiple Points

- Databento - Pairs Trading Example

- Rust std - f64 Primitive

- Hudson & Thames - Distance Approach Documentation

- GitHub - trading-algorithms-rust

- docs.rs - linreg crate

- Rust Book - References and Borrowing

- Stack Overflow - How to Interpret adfuller Test Results

- lib.rs - arima crate

- Econometrics with R - Cointegration

- DolphinDB - adfuller Function

- docs.rs - arima crate (latest)

- Wikipedia - Cointegration

MarketMaker.cc Team

البحوث والاستراتيجيات الكمية