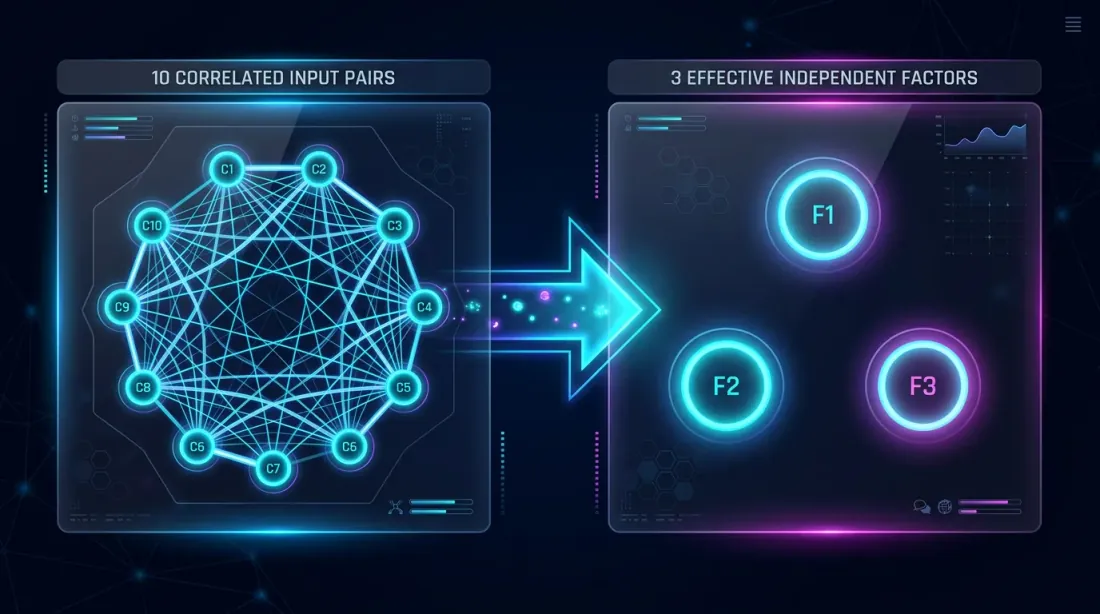

シグナル相関:何ペア監視すべきか

10個の暗号通貨ペアで戦略を立ち上げます:BTC/USDT、ETH/USDT、SOL/USDT、AVAX/USDTなど。ロジックは完璧に見えます:1ペアで戦略がアクティブな時間が5%なら、10ペアでは少なくとも1つがアクティブである時間は。稼働率が4倍になるはずです。

実際には、稼働率は40%ではなく15-16%です。10ペアが3ペアのように振る舞います。資本は遊休し、fill_efficiencyは低下し、実効ポートフォリオリターンは予測の3分の1になります。

原因はシグナル相関です。そして暗号通貨では、それは壊滅的に高いのです。

暗号通貨における分散の幻想

伝統的な金融では、Apple株と石油ETFが異なる要因に反応するため、分散が機能します。暗号通貨市場では、すべてが異なります。

BTCが支配的な要因です。ビットコインが5%下落すると、ETHは6-8%下落し、SOLは8-12%下落し、アルトコインは10-20%下落します。暗号通貨市場における日次リターンの相関は一貫して0.6を超え、パニック時には1.0に近づきます。

しかし、アルゴトレーダーである私たちにとって重要なのは、価格の相関ではなくシグナルの相関です。戦略がモメンタムに基づいていて、BTCがエントリーシグナルをトリガーした場合、ETHとSOLも同じ分以内に類似のシグナルをトリガーする確率が高いです。すべてのペアが同時にロングに入り、同時に退出します。10ポジション — しかし本質的には1つの賭けです。

なぜ10ペア ≠ 10倍の分散なのか

形式的な定式化

各ペアで戦略が時間の割合アクティブであるとします。シグナルが完全に独立であれば、少なくとも1ペアがアクティブである確率:

戦略B(、)の場合:

しかし、シグナルは独立ではありません。暗号通貨は同期して動きます — つまり、シグナルはクラスターで発生し消滅します。

相関が10ペアを3ペアに変える

直感はこうです:10ペアが相関している場合、10の独立したソースではなく、3-4のソースからの情報を持っています。これをeffective_Nを通じて形式化します:

ここではcorrelation factorであり、平均ペアワイズシグナル相関を反映します。のときペアは完全に独立、のとき同一です。

暗号通貨ペアの場合、典型的な。すると:

40%ではなく15.6%。2.5倍の差です。Fill efficiencyもそれに応じて低下し、ポートフォリオ全体の実効リターンも低下します(PnL per Active Timeを参照)。

暗号通貨市場における相関

支配的要因としてのBTC

暗号通貨市場は顕著なファクター構造を持っています。BTCはほとんどのアルトコインの日次リターン分散の60-80%を説明します。これはPCA(主成分分析)を通じて明確に見ることができます:

import numpy as np

from sklearn.decomposition import PCA

def analyze_crypto_factor_structure(returns_matrix: np.ndarray, pair_names: list) -> dict:

"""

PCA analysis of the factor structure of crypto returns.

Args:

returns_matrix: returns matrix [n_days x n_pairs]

pair_names: list of pair names

"""

pca = PCA()

pca.fit(returns_matrix)

explained = pca.explained_variance_ratio_

cumulative = np.cumsum(explained)

print("Factor structure:")

for i, (var, cum) in enumerate(zip(explained[:5], cumulative[:5])):

print(f" PC{i+1}: {var:.1%} variance (cumulative: {cum:.1%})")

loadings = pca.components_[0]

print("\nPC1 loadings (BTC factor):")

for name, load in sorted(zip(pair_names, loadings), key=lambda x: -abs(x[1])):

print(f" {name}: {load:.3f}")

return {

"explained_variance": explained,

"n_effective_factors": int(np.searchsorted(cumulative, 0.90)) + 1,

"pc1_loadings": dict(zip(pair_names, loadings)),

}

10個の暗号通貨ペアのポートフォリオの典型的な結果:

| コンポーネント | 説明分散 | 累積 |

|---|---|---|

| PC1 (BTC) | 65% | 65% |

| PC2 | 12% | 77% |

| PC3 | 8% | 85% |

| PC4 | 5% | 90% |

| PC5-PC10 | 10% | 100% |

4つのファクターが分散の90%を説明します。10ペアのうち、「独立」しているのは最大4つです。

シグナル相関と価格相関の違い

重要なニュアンスがあります。価格の相関とシグナルの相関は異なるものです。BTCとETHの価格相関は0.85ですが、特定の戦略のシグナル相関はエントリーロジックに応じて0.95にも0.50にもなり得ます。

例:RSIの買われすぎ/売られすぎ戦略。BTCのRSIが30を下回る(売られすぎ)— ロングでエントリー。ETHも同じ瞬間に売られすぎかもしれません(シグナル相関0.90)。あるいは、ETHがより緩やかに下落していた場合、そうでないかもしれません(シグナル相関0.40)。

正しいアプローチは、価格系列ではなく、シグナルそのものの相関を測定することです:

import numpy as np

from itertools import combinations

def signal_correlation_matrix(

signals: dict, # {pair: np.array of 0/1 per minute}

method: str = "pearson",

) -> np.ndarray:

"""

Calculate the signal correlation matrix (binary: 0 = flat, 1 = in position).

Args:

signals: dictionary {pair_name: binary_signal_array}

method: correlation method ("pearson", "jaccard")

"""

pairs = sorted(signals.keys())

n = len(pairs)

corr_matrix = np.ones((n, n))

for i, j in combinations(range(n), 2):

s_i = signals[pairs[i]]

s_j = signals[pairs[j]]

if method == "pearson":

corr = np.corrcoef(s_i, s_j)[0, 1]

elif method == "jaccard":

intersection = np.sum(s_i & s_j)

union = np.sum(s_i | s_j)

corr = intersection / union if union > 0 else 0

else:

raise ValueError(f"Unknown method: {method}")

corr_matrix[i, j] = corr

corr_matrix[j, i] = corr

return corr_matrix, pairs

def estimate_correlation_factor(corr_matrix: np.ndarray) -> float:

"""

Estimate correlation_factor from the signal correlation matrix.

correlation_factor = 1 + (N-1) * mean_pairwise_correlation

When correlation is 0 → C_f = 1 (all independent).

When correlation is 1 → C_f = N (all identical).

"""

n = corr_matrix.shape[0]

upper_triangle = corr_matrix[np.triu_indices(n, k=1)]

mean_corr = np.mean(upper_triangle)

correlation_factor = 1 + (n - 1) * mean_corr

return correlation_factor

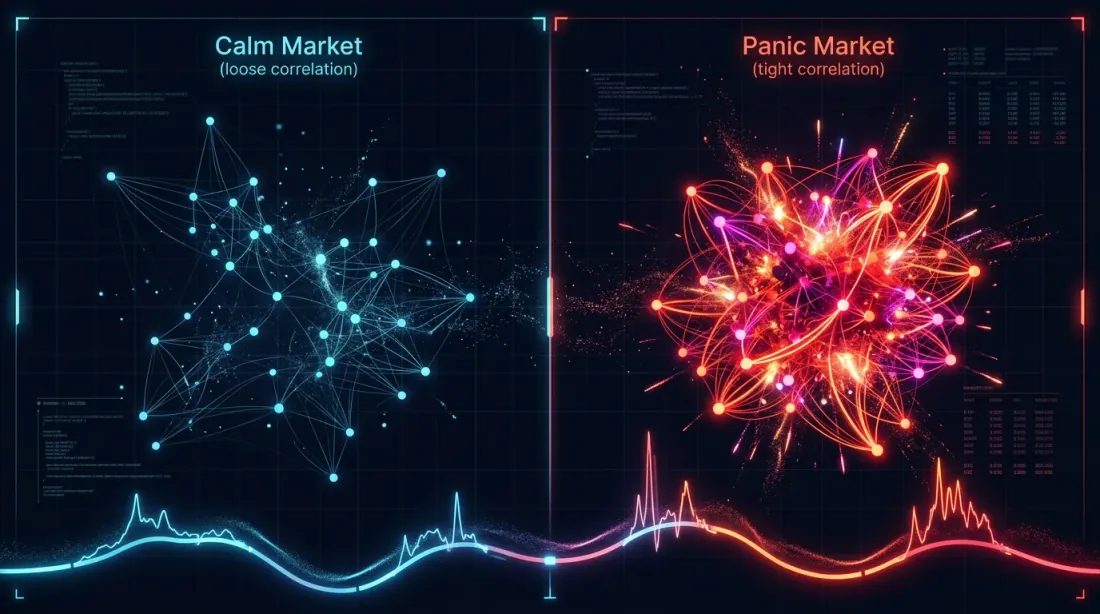

時間的相関:平常時 vs. パニック時

相関は静的ではありません。平常期間中、BTCとアルトコインは乖離する可能性があります — ETHはイーサリアムのニュースで上昇し、SOLはソラナのニュースで上昇します。危機時には、すべてが単一のファクターに崩壊します:リスクオン/リスクオフ。

def rolling_correlation_factor(

signals: dict,

window_days: int = 30,

step_days: int = 7,

) -> list:

"""

Rolling correlation_factor to detect regime changes.

"""

pairs = sorted(signals.keys())

minutes_per_day = 1440

window = window_days * minutes_per_day

step = step_days * minutes_per_day

total_minutes = len(signals[pairs[0]])

results = []

for start in range(0, total_minutes - window, step):

end = start + window

window_signals = {p: signals[p][start:end] for p in pairs}

corr_matrix, _ = signal_correlation_matrix(window_signals)

cf = estimate_correlation_factor(corr_matrix)

results.append({

"start_minute": start,

"end_minute": end,

"correlation_factor": cf,

"effective_n": len(pairs) / cf,

})

return results

10個の暗号通貨ペアの典型的な様相:

| 市場レジーム | 平均シグナル相関 | ||

|---|---|---|---|

| レンジ相場(低ボラティリティ) | 0.15-0.25 | 2.4-3.3 | 3.0-4.2 |

| 上昇トレンド | 0.25-0.40 | 3.3-4.6 | 2.2-3.0 |

| 下降トレンド | 0.30-0.50 | 3.7-5.5 | 1.8-2.7 |

| パニック(暴落) | 0.60-0.90 | 6.4-9.1 | 1.1-1.6 |

パニック時には、10ペアが1-2の実効ペアに圧縮されます。分散が最も必要なときに、それが消失するのです。これは古典的な「危機時には相関が1に向かう」の暗号通貨版です。

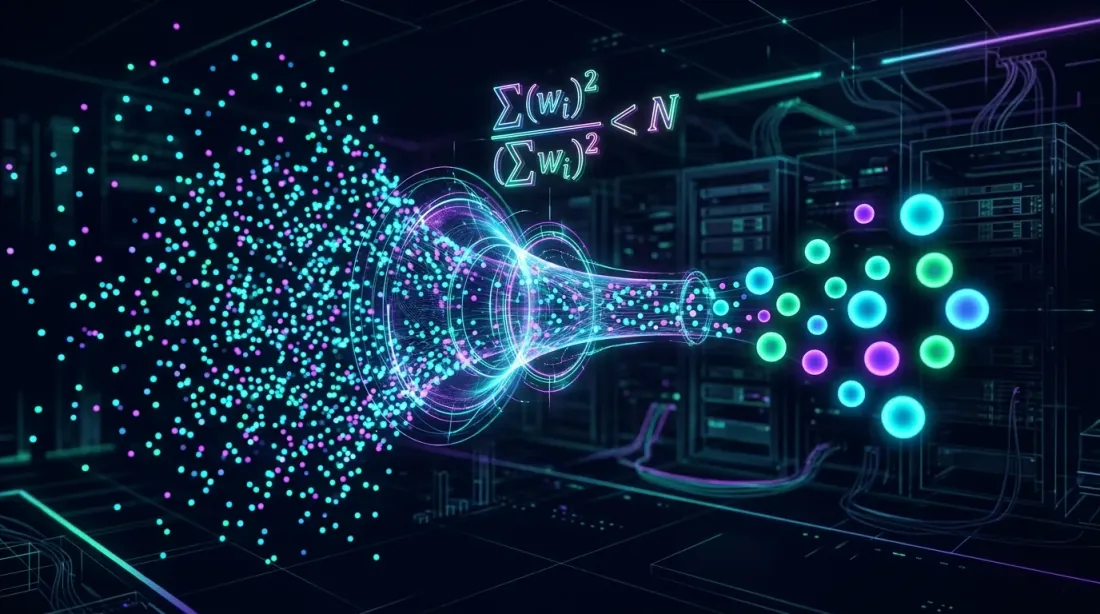

effective_N:核心概念

公式と導出

effective_Nのアイデアは統計学から借用したもので、有効標本サイズが観測値の自己相関を考慮するものです。我々の目的では:

ここでは平均ペアワイズシグナル相関です。簡略表記:

性質:

- のとき:、 — 完全独立

- のとき:、 — すべてのペアが同一

- かつのとき:、

データからcorrelation_factorを推定する方法

実践では3つのアプローチがあります:

1. シグナル相関行列から(正確)。

すべてのペアで戦略を実行し、バイナリシグナル(各分ごとの0/1)を取得し、相関行列を構築し、上記の公式を使ってを計算します。

2. 価格リターンのPCAから(近似)。

シグナルが価格ダイナミクス(モメンタム、平均回帰)に強く依存する場合、を分散の90%を説明するPCAコンポーネント数として推定できます。

3. 資産クラスのヒューリスティクスから(概算)。

| 資産クラス | 典型的な |

|---|---|

| 暗号通貨(トップ10) | 2.5-4.0 |

| 暗号通貨(DeFi/ミームコイン含む) | 2.0-3.0 |

| 外国為替(メジャー) | 1.5-2.5 |

| 株式(単一セクター) | 2.0-3.5 |

| 株式(クロスセクター) | 1.2-1.8 |

BTC、ETH、SOL、AVAX、MATIC、DOGE、DOT、LINK、UNI、ATOMの暗号通貨ポートフォリオの場合、安全な推定値はです。

スロット稼働率モデリング

の公式

相関を考慮した基本公式:

異なる戦略とペア数の表():

| 戦略 | (取引時間) | 5ペア() | 10ペア() | 20ペア() | 50ペア() |

|---|---|---|---|---|---|

| 戦略B | 5% | 8.2% | 15.6% | 29.1% | 58.0% |

| 戦略A | 15% | 23.6% | 41.8% | 65.9% | 92.8% |

| 戦略C | 45% | 67.1% | 89.0% | 98.8% | ~100% |

5%のアクティビティの戦略Bでは、少なくとも1つのアクティブポジションが半分の時間ある状態にするために50ペアが必要です。しかも、50の暗号通貨ペアは10より強く相関しているという事実を考慮していません。

マルチスロットオーケストレーター

実際のオーケストレーターは複数のスロットを同時に管理します。5スロットと10ペアがある場合、稼働率の計算は異なります:

def estimate_fill_efficiency(

trading_time_pct: float,

n_pairs: int,

correlation_factor: float = 3.0,

max_slots: int = 1,

) -> dict:

"""

Analytical estimate of fill efficiency for a multi-slot orchestrator.

Args:

trading_time_pct: fraction of active time for one strategy on one pair

n_pairs: number of trading pairs

correlation_factor: signal correlation coefficient

max_slots: maximum number of simultaneous positions

Returns:

dict with utilization metrics

"""

effective_n = n_pairs / correlation_factor

p_at_least_one = 1 - (1 - trading_time_pct) ** effective_n

expected_active = effective_n * trading_time_pct

utilization = min(expected_active, max_slots) / max_slots

fill_efficiency = min(p_at_least_one, utilization)

return {

"effective_n": effective_n,

"p_at_least_one": p_at_least_one,

"expected_active": expected_active,

"utilization": utilization,

"fill_efficiency": fill_efficiency,

}

configs = [

("Strategy B, 10 pairs, 1 slot", 0.05, 10, 3.0, 1),

("Strategy B, 10 pairs, 3 slots", 0.05, 10, 3.0, 3),

("Strategy B, 30 pairs, 1 slot", 0.05, 30, 3.0, 1),

("Strategy A, 10 pairs, 1 slot", 0.15, 10, 3.0, 1),

("Strategy C, 10 pairs, 1 slot", 0.45, 10, 3.0, 1),

("Strategy C, 10 pairs, 5 slots", 0.45, 10, 3.0, 5),

]

for name, p, n, cf, slots in configs:

result = estimate_fill_efficiency(p, n, cf, slots)

print(f"{name}:")

print(f" N_eff = {result['effective_n']:.1f}")

print(f" P(≥1 active) = {result['p_at_least_one']:.1%}")

print(f" E[active] = {result['expected_active']:.2f}")

print(f" fill_efficiency = {result['fill_efficiency']:.1%}")

print()

期待される出力:

Strategy B, 10 pairs, 1 slot:

N_eff = 3.3

P(≥1 active) = 15.6%

E[active] = 0.17

fill_efficiency = 15.6%

Strategy B, 10 pairs, 3 slots:

N_eff = 3.3

P(≥1 active) = 15.6%

E[active] = 0.17

fill_efficiency = 5.6%

Strategy B, 30 pairs, 1 slot:

N_eff = 10.0

P(≥1 active) = 40.1%

E[active] = 0.50

fill_efficiency = 40.1%

Strategy A, 10 pairs, 1 slot:

N_eff = 3.3

P(≥1 active) = 41.8%

E[active] = 0.50

fill_efficiency = 41.8%

Strategy C, 10 pairs, 1 slot:

N_eff = 3.3

P(≥1 active) = 89.0%

E[active] = 1.50

fill_efficiency = 89.0%

Strategy C, 10 pairs, 5 slots:

N_eff = 3.3

P(≥1 active) = 89.0%

E[active] = 1.50

fill_efficiency = 30.0%

注意:戦略Bの3スロット・10ペアではfill_efficiencyが5.6%です。期待されるアクティブペア数がわずか0.17のとき、3スロットは無意味です。スロットは期待される負荷に比例して割り当てるべきです。

実データからのシミュレーション

分析モデルは近似です。正確な推定にはリアルシグナルでのシミュレーションが必要です:

import numpy as np

def simulate_fill_efficiency(

all_signals: dict, # {(strategy, pair): [(entry_min, exit_min), ...]}

max_slots: int = 10,

test_period_minutes: int = 750 * 24 * 60, # 750 days

priority_fn=None, # priority function for position selection

) -> dict:

"""

Simulate real slot load of the orchestrator.

For each minute: count how many pairs want to enter a position,

and how many slots are actually occupied (accounting for the limit).

Args:

all_signals: signals by pairs and strategies

max_slots: maximum number of simultaneous positions

test_period_minutes: length of the test period in minutes

priority_fn: if None — FIFO; otherwise — ranking function

"""

demand_timeline = np.zeros(test_period_minutes, dtype=np.int32)

capped_timeline = np.zeros(test_period_minutes, dtype=np.int32)

for signals in all_signals.values():

for entry_min, exit_min in signals:

if entry_min < test_period_minutes:

end = min(exit_min, test_period_minutes)

demand_timeline[entry_min:end] += 1

capped_timeline = np.minimum(demand_timeline, max_slots)

total_demand = np.sum(demand_timeline)

total_filled = np.sum(capped_timeline)

time_with_any_active = np.sum(demand_timeline > 0)

fill_efficiency = np.mean(capped_timeline) / max_slots

demand_fill_ratio = total_filled / total_demand if total_demand > 0 else 0

time_utilization = time_with_any_active / test_period_minutes

slot_distribution = {}

for s in range(max_slots + 1):

slot_distribution[s] = np.mean(capped_timeline == s)

return {

"fill_efficiency": fill_efficiency,

"demand_fill_ratio": demand_fill_ratio,

"time_utilization": time_utilization,

"avg_demand": np.mean(demand_timeline),

"avg_filled": np.mean(capped_timeline),

"slot_distribution": slot_distribution,

"overflow_pct": np.mean(demand_timeline > max_slots),

}

リアルデータでのシミュレーションは、分析的推定よりもさらに低い稼働率を示すことが多いです。これは、シグナルの時間的クラスタリングを考慮するためです:すべてのペアがクラスターで同時にエントリーしてオーバーフローを生み出し、その後すべてが沈黙して空白を生み出します。

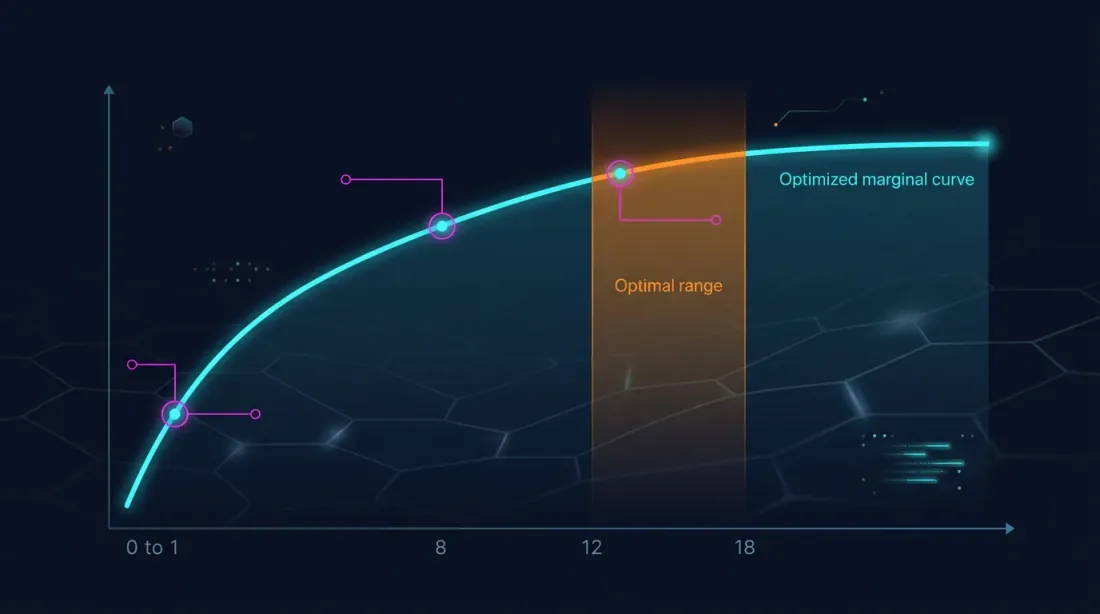

何ペア監視すべきか?収穫逓減分析

重要な問題:どのでもう1ペア追加してもfill_efficiencyが顕著に増加しなくなるのか?

import numpy as np

def diminishing_returns_analysis(

trading_time_pct: float,

correlation_factor: float = 3.0,

max_pairs: int = 100,

target_utilization: float = 0.80,

) -> dict:

"""

Diminishing returns analysis from adding new pairs.

"""

results = []

target_n = None

for n in range(1, max_pairs + 1):

n_eff = n / correlation_factor

p_active = 1 - (1 - trading_time_pct) ** n_eff

marginal = 0

if n > 1:

prev_eff = (n - 1) / correlation_factor

prev_p = 1 - (1 - trading_time_pct) ** prev_eff

marginal = p_active - prev_p

results.append({

"n_pairs": n,

"n_effective": n_eff,

"p_at_least_one": p_active,

"marginal_gain": marginal,

})

if target_n is None and p_active >= target_utilization:

target_n = n

return {

"results": results,

"target_n_for_utilization": target_n,

}

analysis_b = diminishing_returns_analysis(0.05, correlation_factor=3.0, target_utilization=0.80)

print(f"Strategy B: need {analysis_b['target_n_for_utilization']} pairs for 80% P(≥1)")

for r in analysis_b["results"]:

if r["n_pairs"] in [1, 3, 5, 10, 20, 30, 50, 80]:

print(f" N={r['n_pairs']:3d}: N_eff={r['n_effective']:.1f}, "

f"P(≥1)={r['p_at_least_one']:.1%}, "

f"marginal={r['marginal_gain']:.2%}")

戦略B(、)の結果:

| ペア | 限界利得 | ||

|---|---|---|---|

| 1 | 0.3 | 1.7% | — |

| 3 | 1.0 | 5.0% | +1.7% |

| 5 | 1.7 | 8.2% | +1.6% |

| 10 | 3.3 | 15.6% | +1.4% |

| 20 | 6.7 | 29.1% | +1.1% |

| 30 | 10.0 | 40.1% | +0.9% |

| 50 | 16.7 | 58.0% | +0.6% |

| 80 | 26.7 | 74.5% | +0.4% |

戦略Bの場合、80%のシングルスロット稼働率に到達することは100ペアでも不可能です(~96ペアが必要)。これは根本的な制約です:取引時間5%の戦略はシングルスロット運用には適していません — 複数の戦略を組み合わせたポートフォリオアプローチが必要です。

戦略A(、)の場合:

| ペア | 限界利得 | ||

|---|---|---|---|

| 5 | 1.7 | 23.6% | — |

| 10 | 3.3 | 41.8% | +3.3% |

| 20 | 6.7 | 65.9% | +2.1% |

| 30 | 10.0 | 80.3% | +1.2% |

戦略Aは~30ペアで80%の稼働率に到達します。30番目のペアの限界利得はわずか+1.2%です。

戦略C(、)の場合:

| ペア | ||

|---|---|---|

| 3 | 1.0 | 45.0% |

| 5 | 1.7 | 67.1% |

| 10 | 3.3 | 89.0% |

| 15 | 5.0 | 95.0% |

取引時間45%の戦略Cは、わずか10ペアで90%の稼働率に到達します。それ以上追加しても意味がありません。

ペア間のエッジ劣化

ペア数を制限するもう一つの要因があります:エッジの劣化。BTC/USDTで開発・最適化された戦略は、流動性の低いアルトコインではパフォーマンスが低下する可能性があります。

劣化の原因:

- 流動性:DOGE/USDTのスリッページはBTC/USDTの数倍

- スプレッド:流動性の低いペアはビッド・アスクスプレッドが広い

- マイクロストラクチャー:オーダーブックのパターンはペアによって異なる

- マニピュレーション:低流動性のアルトコインはポンプ・アンド・ダンプの影響を受けやすい

def edge_decay_analysis(

strategy_results: dict, # {pair: {"pnl_per_day": float, "n_trades": int}}

min_trades: int = 30,

) -> list:

"""

Rank pairs by edge accounting for degradation.

"""

ranked = []

for pair, metrics in strategy_results.items():

if metrics["n_trades"] < min_trades:

continue

ranked.append({

"pair": pair,

"pnl_per_day": metrics["pnl_per_day"],

"n_trades": metrics["n_trades"],

"sharpe": metrics.get("sharpe", 0),

})

ranked.sort(key=lambda x: x["pnl_per_day"], reverse=True)

cumulative_pnl = []

running_sum = 0

for i, r in enumerate(ranked):

running_sum += r["pnl_per_day"]

avg = running_sum / (i + 1)

cumulative_pnl.append({

"n_pairs": i + 1,

"last_added": r["pair"],

"last_pnl_per_day": r["pnl_per_day"],

"avg_pnl_per_day": avg,

})

return cumulative_pnl

典型的な様相:

| ペア数 | 最後に追加 | 最後のPnL/日 | 平均PnL/日 |

|---|---|---|---|

| 1 | BTC/USDT | 0.89% | 0.89% |

| 2 | ETH/USDT | 0.82% | 0.86% |

| 3 | SOL/USDT | 0.71% | 0.81% |

| 5 | AVAX/USDT | 0.55% | 0.73% |

| 8 | DOT/USDT | 0.31% | 0.61% |

| 10 | DOGE/USDT | 0.12% | 0.53% |

10番目のペアを追加すると、ポートフォリオの平均PnL/日が下がります。8番目のペアの時点で、エッジはすでにベストの半分です。fill_efficiency(ペア数とともに増加)と平均エッジ(低下する)のバランスが必要です。

最適ペア数:統一モデル

fill_efficiencyとエッジ劣化を単一の指標 — 期待ポートフォリオPnL/日 — に統合します:

def optimal_pairs_count(

pair_edges: list, # PnL/day in descending order: [0.89, 0.82, 0.71, ...]

trading_time_pct: float,

correlation_factor: float = 3.0,

max_slots: int = 1,

) -> dict:

"""

Find the optimal number of pairs that maximizes portfolio PnL.

"""

best_n = 0

best_score = 0

results = []

for n in range(1, len(pair_edges) + 1):

avg_edge = np.mean(pair_edges[:n])

n_eff = n / correlation_factor

p_active = 1 - (1 - trading_time_pct) ** n_eff

expected_active = n_eff * trading_time_pct

utilization = min(expected_active, max_slots) / max_slots

fill_eff = min(p_active, utilization)

portfolio_score = avg_edge * fill_eff * 365

results.append({

"n_pairs": n,

"avg_edge": avg_edge,

"fill_efficiency": fill_eff,

"portfolio_annualized": portfolio_score,

})

if portfolio_score > best_score:

best_score = portfolio_score

best_n = n

return {

"optimal_n": best_n,

"optimal_score": best_score,

"results": results,

}

edges = [0.89, 0.82, 0.71, 0.65, 0.55, 0.48, 0.40, 0.31, 0.22, 0.12,

0.08, 0.05, 0.02, -0.01, -0.05]

opt = optimal_pairs_count(edges, trading_time_pct=0.15, correlation_factor=3.0)

print(f"Optimal number of pairs: {opt['optimal_n']}")

print(f"Portfolio annualized: {opt['optimal_score']:.1f}%")

for r in opt["results"]:

print(f" N={r['n_pairs']:2d}: avg_edge={r['avg_edge']:.2f}%, "

f"fill_eff={r['fill_efficiency']:.1%}, "

f"portfolio={r['portfolio_annualized']:.1f}%")

最適値は通常、ペア追加による限界fill_efficiencyが平均エッジの低下を補えなくなるポイントにあります。典型的な暗号通貨ポートフォリオの場合:

- 戦略B(5%時間):最適は8-12ペア

- 戦略A(15%時間):最適は6-10ペア

- 戦略C(45%時間):最適は4-6ペア

パラドックス:取引時間が最も短い戦略が最も多くのペアから恩恵を受けますが、fill_efficiencyは依然として低いままです。解決策はペアを増やすことではなく、他の戦略との組み合わせです(コンボ戦略を参照)。

クロスペア分散:相関削減戦略

ペア数を無限に増やせないなら、を下げる — つまりシグナルの多様性を高めることができます。

戦略1:流動性の高いトークンとDeFiトークンのミックス

BTC、ETH、BNBは非常に強く相関しています。しかし、UNI(DEX)、AAVE(レンディング)、CRV(ステーブルコイン)は独自のドライバーを持つ可能性があります。DeFiトークンを追加すると、平均が0.35から0.20-0.25に低下します:

戦略2:同じペアに異なる戦略

1つの戦略で10ペアではなく — 2つの異なる戦略で5ペア。戦略が異なる原理に基づいている場合(モメンタム vs. 平均回帰)、シグナルは逆相関になり得ます:

- モメンタムは価格上昇時にロングエントリー

- 平均回帰は価格下落時にロングエントリー

これはを達成する唯一の方法です — 負のシグナル相関を持つ戦略を使用することです。

戦略3:現物 vs. 先物

ファンディングレート裁定取引と現物取引は異なる相関構造を持っています。裁定戦略をポートフォリオに追加すると、全体のが大幅に低下します。裁定取引は定義上、収束ではなく乖離を利用するためです。

戦略タイプ別の実践的推奨事項

高頻度・低時間戦略(取引時間 < 10%)

典型的な代表:戦略B(5%時間、750日間で38トレード)。

- ペア数:10-15(エッジ/稼働バランスの最適値)

- 問題:15ペアでもfill_efficiencyは低い(~20-25%)

- 解決策:オーケストレーターで他の戦略との組み合わせが必須

- 暗号通貨の:2.5-3.5

- モニタリング:ローリングで市場レジームに応じたペア数の適応

中時間戦略(取引時間10-30%)

典型的な代表:戦略A(15%時間、750日間で418トレード)。

- ペア数:6-10

- 10ペアでのFill_efficiency:~40%

- 解決策:このような戦略を2-3組み合わせると80%以上の時間を埋められる

- 暗号通貨の:2.5-3.5

- 重点:最大エッジのペアを選択し、数を追わない

高時間戦略(取引時間 > 30%)

典型的な代表:戦略C(45%時間)。

- ペア数:4-6

- 6ペアでのFill_efficiency:~80%

- 問題:オーバーフロー — 複数ペアが同時にアクティブだがスロットが足りない

- 解決策:max_slotsを増やすかペア優先順位付けを追加

- 暗号通貨の:2.5-4.0(ロングポジションが危機と重なるため高い)

サマリーテーブル

| パラメータ | 戦略B(5%) | 戦略A(15%) | 戦略C(45%) |

|---|---|---|---|

| 推奨 | 10-15 | 6-10 | 4-6 |

| での | 3.3-5.0 | 2.0-3.3 | 1.3-2.0 |

| Fill eff.(1スロット) | 15-23% | 32-42% | 77-89% |

| 組み合わせ必要? | 必須 | 望ましい | 不要 |

| ボトルネック | シグナル不足 | バランス | オーバーフロー |

シリーズの他の指標との関連

この記事は「幻想なきバックテスト」シリーズの第11回です。シグナル相関は、前回の記事の指標に直接影響します:

-

PnL per Active Time: fill_efficiencyは実効リターン公式の主要な乗数です。相関を無視してfill_efficiencyを過大評価すると、ポートフォリオのPnL予測が過度に楽観的になります。

-

ファンディングレート: 高相関ではポジションが同時にオープンし、ファンディングコストはスロット数に比例して増大します。オーバーフロー + ファンディング = 資本の加速的な消耗。

-

ファンディングレート裁定: 裁定戦略はポートフォリオのを低下させる自然な分散要素です。そのシグナルはモメンタムや平均回帰戦略との相関が弱いです。

-

コンボ戦略(次の記事):異なるとを持つ戦略のポートフォリオを組み立てて90%以上の稼働率を達成する方法。カスケードオーケストレーションは優先度を割り当てる際にシグナル相関を考慮します。

結論

暗号通貨における分散はペア数の問題ではありません。10の相関ペアは3-4の独立したペアの効果しかもたらしません。パニック時にはさらに少なくなります。

4つの要点:

-

Nではなくeffective_Nを計算せよ。 暗号通貨ペアの。10ペアは~3.3の実効ペアです。fill_efficiencyはではなくに基づいて計画してください。

-

価格相関ではなくシグナル相関を測定せよ。 価格相関はプロキシであり、代替ではありません。すべてのペアで戦略を実行し、バイナリシグナル相関行列を計算してください。

-

エッジの劣化を考慮せよ。 ペアが増えると平均PnL/日が下がります。最適点は、新しいペアからの限界fill_efficiencyがエッジの低下を補えるポイントです。

-

を増やすのではなくを下げよ。 同じペアに異なる戦略を組み合わせる方が、1つの戦略をより多くのペアに適用するより効果的です。クロス戦略の分散はを達成できます。

Correlation factorは、稼働率とリターン予測がどれほど現実的かを決定する隠れた変数です。これを無視することは、幻想の上にポートフォリオを構築することを意味します。

参考リンク

- Markowitz, H. — Portfolio Selection (1952)

- López de Prado — Advances in Financial Machine Learning: Denoising and Detoning

- Ledoit, O. & Wolf, M. — Honey, I Shrunk the Sample Covariance Matrix (2004)

- Laloux, L. et al. — Noise Dressing of Financial Correlation Matrices (1999)

- Cont, R. — Empirical Properties of Asset Returns: Stylized Facts and Statistical Issues

- Ernest Chan — Algorithmic Trading: Portfolio Construction and Risk Management

- Rebonato, R. & Jäckel, P. — The Most General Methodology for Creating a Valid Correlation Matrix

Citation

@article{soloviov2026signalcorrelation,

author = {Soloviov, Eugen},

title = {Signal Correlation: How Many Pairs to Monitor},

year = {2026},

url = {https://marketmaker.cc/ru/blog/post/signal-correlation-pairs},

version = {0.1.0},

description = {Why 10 crypto pairs don't provide 10x diversification, how to calculate effective\_N via correlation\_factor, and how many pairs you really need to monitor for 80-90\% orchestrator slot utilization.}

}

MarketMaker.cc Team

クオンツ・リサーチ&戦略