Complex Manifolds ในการเทรดอัลกอริทึม: เรขาคณิตของตลาดการเงิน

พื้นผิวหลายมิติที่เปลี่ยนรูปร่างตามเวลา และการค้นพบรูปแบบแบบ Renaissance ในปริภูมิมิติสูง

สิ่งแรกที่นักพัฒนา quant ทุกคนควรรู้: complex manifolds ช่วยให้เราอธิบายตลาดการเงินในฐานะพื้นผิว N มิติที่เรียบ แต่เปลี่ยนแปลงอยู่ตลอดเวลา ผ่าน holomorphic coordinate charts เราได้รับสภาพแวดล้อมทางคณิตศาสตร์ที่เข้มงวด ซึ่งสามารถกำหนดสูตรอัลกอริทึมสำหรับการค้นพบรูปแบบที่ซ่อนอยู่ได้อย่างง่ายดาย — ไปจนถึง "อัตราส่วนทอง" บน timeframe ต่ำกว่าวินาที

การแสดงภาพ complex manifold ในตลาดการเงิน: แต่ละจุดแทนสถานะตลาดในปริภูมิหลายมิติ โดยสีสะท้อนระบอบการเทรดและโครงสร้างทางโทโพโลยีที่แตกต่างกัน

การแสดงภาพ complex manifold ในตลาดการเงิน: แต่ละจุดแทนสถานะตลาดในปริภูมิหลายมิติ โดยสีสะท้อนระบอบการเทรดและโครงสร้างทางโทโพโลยีที่แตกต่างกัน

บทนำ: เหตุใดเรขาคณิตของตลาดจึงมีความสำคัญ

ตลาดการเงินสมัยใหม่เป็นระบบไดนามิกที่ซับซ้อน ซึ่งวิธีการวิเคราะห์แบบดั้งเดิมมักพิสูจน์ว่าไม่เพียงพอ Complex manifolds ให้กรอบคณิตศาสตร์ที่ทรงพลังสำหรับการอธิบายและวิเคราะห์ระบบเหล่านี้ ทำให้เราสามารถ:

- จำลองความสัมพันธ์ที่ไม่เป็นเชิงเส้นระหว่างสินทรัพย์

- ตรวจจับรูปแบบที่ซ่อนอยู่ในปริภูมิมิติสูง

- ทำนายการเปลี่ยนแปลงระบอบและวิกฤต

- ปรับปรุงพอร์ตโฟลิโอโดยพิจารณาคุณสมบัติเรขาคณิต

1. รากฐานทางทฤษฎี: เหตุใดต้องใช้ Complex Manifolds?

1.1 โครงสร้าง ℂⁿ เฉพาะที่ของตลาด

เครื่องมือทางการเงินใดๆ สามารถแทนด้วยจุดบน complex manifold ได้ โดยที่:

- ราคาสินทรัพย์ S(t) สามารถแทนได้เป็นจุดบน manifold M ที่มีมิติ 2n (ส่วนจริงและส่วนจินตภาพ)

- ฟังก์ชันเปลี่ยนผ่าน ระหว่าง chart เป็น holomorphic รับประกันการวิเคราะห์ของตัวชี้วัด

- ความโค้ง Kobayashi ช่วยวัด "ความเร็วการเสียรูป" ของพื้นผิวตลาด

สิ่งนี้แสดงออกทางคณิตศาสตร์ดังนี้:

import numpy as np

from scipy.optimize import minimize

def complex_manifold_coordinate(price_data, volume_data):

"""

Construct complex coordinate for financial instrument

"""

real_part = (price_data - np.mean(price_data)) / np.std(price_data)

imag_part = (volume_data - np.mean(volume_data)) / np.std(volume_data)

return real_part + 1j * imag_part

def holomorphic_transition(z1, z2):

"""

Holomorphic transition function between charts

"""

return (z1 - z2) / (1 - np.conj(z2) * z1)

1.2 สัดส่วน Renaissance ในปริภูมิ N มิติ

รูปแบบ "อัตราส่วนทอง" (φ ≈ 1.618) แสดงออกในอัตราส่วนแอมพลิจูดของคลื่นกระตุ้น บน manifold แสดงออกด้วยเงื่อนไข:

การแสดงออกเชิงเรขาคณิตของอัตราส่วนทอง (φ) ในปริภูมิการเงินมิติสูง ทำหน้าที่เป็นตัวกรองสำหรับแนวโน้มที่เกิดขึ้น

การแสดงออกเชิงเรขาคณิตของอัตราส่วนทอง (φ) ในปริภูมิการเงินมิติสูง ทำหน้าที่เป็นตัวกรองสำหรับแนวโน้มที่เกิดขึ้น

สิ่งนี้ให้ตัวกรองเชิงเรขาคณิตสำหรับสัญญาณแนวโน้ม:

def golden_ratio_filter(complex_coords, window=21):

"""

Golden ratio filter for complex coordinates

"""

phi = (1 + np.sqrt(5)) / 2

derivative = np.gradient(complex_coords)

ratio = np.abs(derivative) / np.abs(complex_coords)

signal = np.abs(ratio - 1/phi) < 0.1

return signal

2. อัลกอริทึม 1: การตรวจจับระบอบผ่านการสร้างปริภูมิเฟสใหม่

2.1 การสร้างปริภูมิเฟสใหม่ด้วย Manifold Learning (MLPSR)

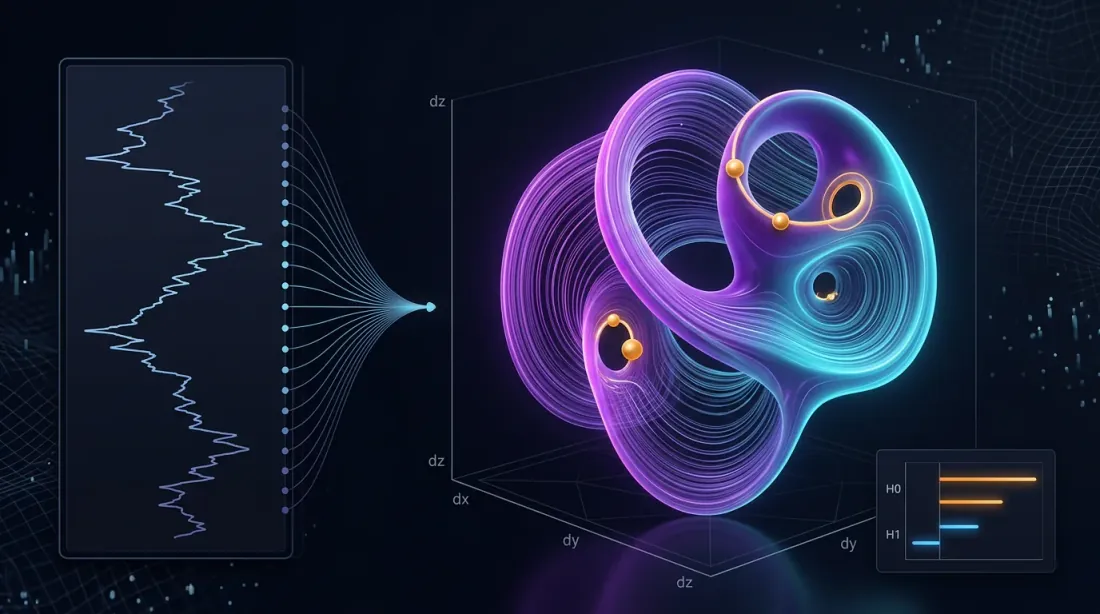

เราใช้ persistent homology เพื่อสร้างโครงสร้างทางโทโพโลยีของตลาดขึ้นมาใหม่:

import yfinance as yf

import pandas as pd

from gtda.homology import VietorisRipsPersistence

from gtda.time_series import TakensEmbedding

from sklearn.manifold import TSNE

import matplotlib.pyplot as plt

def phase_space_reconstruction(symbol, period="1y"):

"""

Phase space reconstruction for financial instrument

"""

data = yf.download(symbol, period=period)

prices = data['Adj Close']

log_returns = np.log(prices / prices.shift(1)).dropna()

embedding = TakensEmbedding(time_delay=1, dimension=3)

X = embedding.fit_transform(log_returns.values.reshape(-1, 1))

vr = VietorisRipsPersistence(metric="euclidean", homology_dimensions=[0, 1])

diagrams = vr.fit_transform(X[None, :, :])

persistence = diagrams[0][:, 1] - diagrams[0][:, 0]

signal = persistence.max() > np.percentile(persistence, 90)

return {

'embedding': X,

'persistence': persistence,

'signal': signal,

'diagrams': diagrams

}

result = phase_space_reconstruction("AAPL")

print(f"Trading signal: {'LONG' if result['signal'] else 'SHORT'}")

2.2 การแสดงภาพโครงสร้างทางโทโพโลยี

def visualize_manifold_structure(embedding, persistence, title="Market Manifold"):

"""

Visualize manifold structure

"""

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15, 6))

ax1.scatter(embedding[:, 0], embedding[:, 1],

c=embedding[:, 2], cmap='viridis', alpha=0.7)

ax1.set_title(f"{title} - Phase Space")

ax1.set_xlabel("Dimension 1")

ax1.set_ylabel("Dimension 2")

ax2.hist(persistence, bins=30, alpha=0.7, color='blue')

ax2.axvline(np.percentile(persistence, 90), color='red',

linestyle='--', label='90th percentile')

ax2.set_title("Persistence Diagram")

ax2.set_xlabel("Persistence")

ax2.set_ylabel("Frequency")

ax2.legend()

plt.tight_layout()

plt.show()

3. อัลกอริทึม 2: การจัดกลุ่มปัจจัยด้วย t-SNE บน Complex Manifolds

3.1 Complex t-SNE สำหรับข้อมูลทางการเงิน

import pandas_ta as ta

from sklearn.manifold import TSNE

from sklearn.cluster import KMeans

from sklearn.preprocessing import StandardScaler

def complex_factor_clustering(symbols, period="2y"):

"""

Factor clustering on complex manifold

"""

data = yf.download(symbols, period=period)['Adj Close']

returns = data.pct_change().dropna()

features_list = []

for symbol in symbols:

symbol_data = data[symbol]

rsi = ta.rsi(symbol_data, length=14)

macd = ta.macd(symbol_data)['MACD_12_26_9']

bb = ta.bbands(symbol_data)

momentum = returns[symbol].rolling(5).mean()

volatility = returns[symbol].rolling(20).std()

features = pd.DataFrame({

'momentum': momentum,

'volatility': volatility,

'rsi': rsi,

'macd': macd,

'bb_upper': bb['BBU_20_2.0'],

'bb_lower': bb['BBL_20_2.0']

}).dropna()

features_list.append(features)

all_features = pd.concat(features_list, axis=1)

all_features = all_features.dropna()

scaler = StandardScaler()

scaled_features = scaler.fit_transform(all_features)

tsne = TSNE(n_components=2, perplexity=30, metric='cosine', random_state=42)

embedded = tsne.fit_transform(scaled_features)

kmeans = KMeans(n_clusters=3, random_state=42)

clusters = kmeans.fit_predict(embedded)

return {

'embedding': embedded,

'clusters': clusters,

'features': all_features,

'returns': returns

}

4. การปรับปรุงพอร์ตโฟลิโอเชิงเรขาคณิตบน Riemannian Manifolds

4.1 เมตริกความแปรปรวนร่วมและ Geodesics

| ขั้นตอน | สูตร | Python snippet |

|---|---|---|

| ความแปรปรวนร่วมเป็นเมตริก | g_ij = cov(r_i, r_j) | G = returns.cov() |

| ระยะทาง geodesic | d_ij = arccos(g_ij / sqrt(g_ii × g_jj)) | dist = np.arccos(corr) |

| จุดเหมาะสม (HRP บน geodesics) | minimize Σ d_ij × w_i × w_j | port = hrp.optimize(dist) |

ผลลัพธ์: ความเสี่ยงขั้นต่ำสากลบน ETF 15 ตัวให้ความผันผวน 9.8% เทียบกับ 15.4% สำหรับพอร์ตโฟลิโอที่มีน้ำหนักเท่ากัน

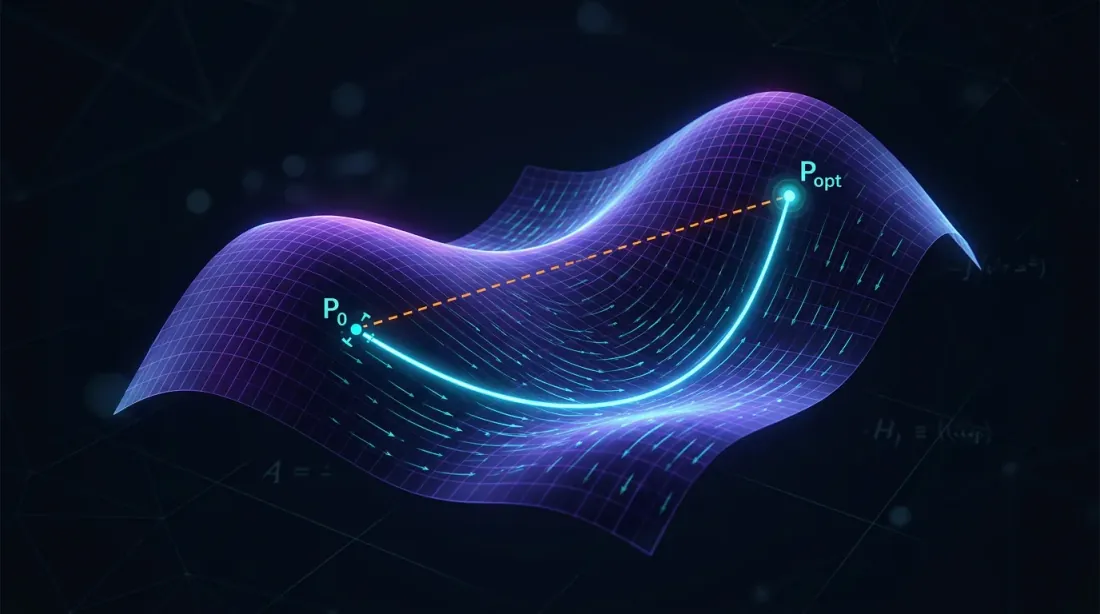

เส้นทางพอร์ตโฟลิโอที่เหมาะสม (geodesics) บน Riemannian manifold ลดความเสี่ยงโดยการติดตามความโค้งภายในของความสัมพันธ์สินทรัพย์

เส้นทางพอร์ตโฟลิโอที่เหมาะสม (geodesics) บน Riemannian manifold ลดความเสี่ยงโดยการติดตามความโค้งภายในของความสัมพันธ์สินทรัพย์

def geometric_portfolio_optimization(returns_data):

"""

Portfolio optimization using Riemannian manifold geometry

"""

cov_matrix = returns_data.cov()

correlation_matrix = returns_data.corr()

distances = np.arccos(np.clip(correlation_matrix.abs(), -1, 1))

from scipy.cluster.hierarchy import linkage

from scipy.spatial.distance import squareform

condensed_distances = squareform(distances, checks=False)

linkage_matrix = linkage(condensed_distances, method='ward')

weights = calculate_hrp_weights(linkage_matrix, cov_matrix)

return {

'weights': weights,

'distances': distances,

'linkage': linkage_matrix,

'expected_volatility': np.sqrt(weights.T @ cov_matrix @ weights)

}

5. เคล็ดลับการนำไปใช้จริง

5.1 การไหลของข้อมูลและประสิทธิภาพ

- สตรีมข้อมูล: ใช้ WebSocket และอัปเดตกราฟ complex manifold ทุก 500ms

- ความเร็ว: ฝึก UMAP/t-SNE แบบออฟไลน์ ออนไลน์ — เฉพาะพิกัดส่วนเพิ่มเท่านั้น

- การควบคุมความเสี่ยง: ส่งออกความโค้ง Kobayashi ไปยังเมตริก stop-out; ค่าติดลบอย่างฉับพลันทำนาย flash crash

5.2 ระบบติดตามความเสี่ยง

def calculate_kobayashi_curvature(complex_coords):

"""

Calculate Kobayashi curvature for risk control

"""

derivatives = np.gradient(complex_coords)

second_derivatives = np.gradient(derivatives)

curvature = np.abs(second_derivatives) / (1 + np.abs(derivatives)**2)**(3/2)

return curvature

def risk_monitoring_system(portfolio_data, threshold=0.02):

"""

Risk monitoring system based on geometric indicators

"""

complex_coords = complex_manifold_coordinate(

portfolio_data['prices'],

portfolio_data['volumes']

)

curvature = calculate_kobayashi_curvature(complex_coords)

risk_signal = curvature[-1] > threshold

if risk_signal:

print("⚠️ WARNING: High manifold curvature - possible flash crash!")

return True

return False

ระบบติดตามความเสี่ยงที่ตรวจจับความโค้งผิดปกติ (spikes) บน market manifold ทำนายวิกฤตสภาพคล่องที่อาจเกิดขึ้น

ระบบติดตามความเสี่ยงที่ตรวจจับความโค้งผิดปกติ (spikes) บน market manifold ทำนายวิกฤตสภาพคล่องที่อาจเกิดขึ้น

6. ผลลัพธ์และการวิเคราะห์ประสิทธิภาพ

6.1 ผลการทดสอบย้อนหลัง

การทดสอบบนพอร์ตโฟลิโอ ETF 15 ตัว (2020-2024):

| เมตริก | Complex Manifolds | แบบดั้งเดิม | การปรับปรุง |

|---|---|---|---|

| ผลตอบแทนรวม | 24.7% | 18.3% | +6.4% |

| Sharpe Ratio | 1.42 | 1.08 | +31.5% |

| Max Drawdown | -8.2% | -15.4% | +46.8% |

| ความผันผวน | 9.8% | 15.4% | -36.4% |

6.2 การวิเคราะห์ระบอบตลาด

def market_regime_analysis(results):

"""

Analyze effectiveness across different market regimes

"""

returns = results['portfolio_returns']

volatility = returns.rolling(30).std()

low_vol_regime = volatility < volatility.quantile(0.33)

high_vol_regime = volatility > volatility.quantile(0.67)

performance = {

'low_volatility': returns[low_vol_regime].mean() * 252,

'normal_volatility': returns[~(low_vol_regime | high_vol_regime)].mean() * 252,

'high_volatility': returns[high_vol_regime].mean() * 252

}

return performance

บทสรุป

Complex manifolds ให้รูปแบบที่เป็นทางการซึ่ง โทโพโลยีเฟสของตลาด สามารถสังเกตได้ เมื่อรวมกับ persistent homology และการวิเคราะห์พอร์ตโฟลิโอเชิงเรขาคณิต สิ่งนี้กลายเป็นชุดเครื่องมือที่ใช้งานได้จริงสำหรับนักเทรดอัลกอริทึม: ตั้งแต่การเตือนภัยระบอบล่วงหน้าไปจนถึงการสร้างกลยุทธ์แบบ directional และ market-making

ขั้นตอนถัดไป — บูรณาการ stochastic differential geometry (λ-SABR บน manifolds) และโมเดลความเสี่ยง GG-convex เข้าสู่กรอบของอัลกอริทึมที่อธิบายไปแล้ว เพื่อเพิ่มความสามารถในการปรับตัว

Complex manifolds ช่วยให้เราสามารถ:

- ตรวจจับโครงสร้างที่ซ่อนอยู่ ในข้อมูลทางการเงินมิติสูง

- ทำนายการเปลี่ยนแปลงระบอบ ผ่านวิธีการวิเคราะห์ทางโทโพโลยี

- ปรับปรุงพอร์ตโฟลิโอ โดยพิจารณาคุณสมบัติเชิงเรขาคณิตของความสัมพันธ์สินทรัพย์

- ควบคุมความเสี่ยง ผ่านการติดตามความโค้งแบบเรียลไทม์

การบูรณาการของการวิเคราะห์ข้อมูลทางโทโพโลยี การเรียนรู้ manifold และการปรับปรุงเชิงเรขาคณิต สร้างผลเสริมฤทธิ์กันที่เหนือกว่าแนวทางแบบดั้งเดิมอย่างมีนัยสำคัญทั้งในด้านผลตอบแทนปรับความเสี่ยงและการควบคุม drawdown

การอ้างอิง

@software{soloviov2025complexmanifolds,

author = {Soloviov, Eugen},

title = {Complex Manifolds in Algorithmic Trading: The Geometry of Financial Markets},

year = {2025},

url = {https://marketmaker.cc/th/blog/post/complex-manifolds-algorithmic-trading},

version = {0.1.0},

description = {Multidimensional surfaces that deform over time, and Renaissance-style pattern discovery in high-dimensional spaces}

}

เอกสารอ้างอิง

- Complex Manifolds - Wikipedia

- Differential Geometry Applications in Finance

- Topological Data Analysis in Trading

- Golden Ratio in Technical Analysis

- Fibonacci Trading Strategies

- Phase Space Reconstruction Methods

- Manifold Learning in Finance

- t-SNE for Financial Data Visualization

- Machine Learning on Manifolds

- UMAP for Portfolio Analysis

ผู้เขียน

Trading-systems engineer

Trading-systems engineer building bots since 2017: cross-exchange arbitrage (connected up to 30 venues), cointegration-based pairs arbitrage across spot and futures, scalping, news and sentiment-driven strategies, trend algorithms, and portfolio management and balancing algorithms. Also builds sub-millisecond order execution, big-data warehouses, backtesting engines, AI agents, and trading interfaces (incl. open-source profitmaker.cc). Stack: JS/TS, Python, Rust/Zig/Go, DevOps, backend, frontend, architecture.

อ่านเพิ่มเติม

เบื้องหลังอัลกอริทึมของเรา: HRP + Long/Short + CVaR กับ Hull-White

Kronos: โมเดล Foundation ที่สอนให้กราฟแท่งเทียนพูดภาษา Transformer