Cascade Strategies: Priority Execution with Fallback Filling

Finale of the "Backtests Without Illusions" series. How to build an orchestrator from N strategies on M pairs, implement cascade mode with priority and fallback execution, choose dual_size, and why strategy portfolios cannot be backtested by simply summing PnL.

Why You Need a Strategy Portfolio

Multiple strategies compete for limited capital — most sit idle while only a few trade at any given time

Multiple strategies compete for limited capital — most sit idle while only a few trade at any given time

You've put a strategy through the full pipeline. Monte Carlo bootstrap showed an acceptable 5th percentile. Walk-forward confirmed out-of-sample returns. Funding rates are accounted for, plateau analysis passed. The strategy genuinely works.

But it trades 15% of the time. The remaining 85% your capital sits idle.

Run a second strategy? A third? A tenth? The idea is obvious. The implementation is not. A strategy portfolio creates problems that don't exist with a single bot:

- Conflicts: two strategies want to open opposite positions on the same pair.

- Constraints: the exchange/risk management allows no more than simultaneous positions.

- Allocation: what fraction of capital to give each strategy?

- Correlation: 10 strategies on correlated crypto pairs is not 10x diversification.

Cascade strategy is an architectural pattern that solves these problems: the primary strategy gets the full position size, while the fallback strategy fills idle time with a reduced position.

The Cascade Concept: Primary + Fallback

High-Conviction Strategy (Primary)

Primary is a strategy with strict entry criteria. For example, triple timeframe with three confirming levels: signal on daily + 4-hour + hourly, with volatility and volume filtering.

Characteristics:

- Few trades (tens over the backtest period)

- High PnL per trade

- Low time in position (5-15%)

- High confidence in each entry

Fallback Strategy

Fallback is a strategy with relaxed criteria. Dual timeframe, fewer filters, wider tolerances. It trades more frequently, but with lower edge per trade.

Characteristics:

- More trades (hundreds over the period)

- Moderate PnL per trade

- High time in position (30-50%)

- Moderate confidence — compensated by reduced position size

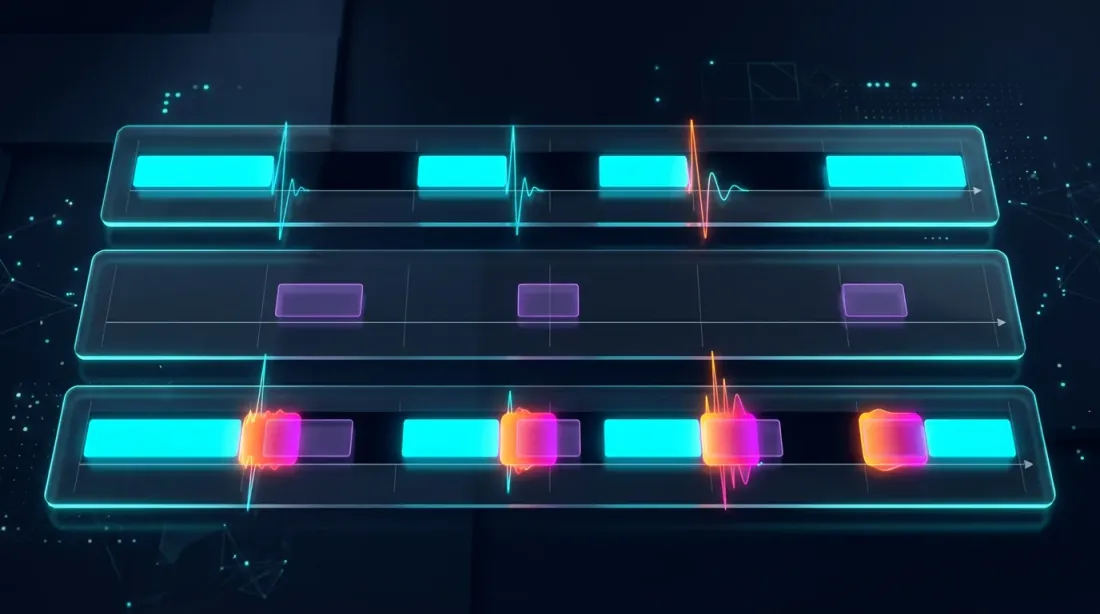

Cascade Mode

timeline: ──────────────────────────────────────────────────

primary: ___████___________________████████____███________

fallback: ███____███████████████████________████___████████

capital: [dual][ full ][ dual_size ][ full ][ dual ]

When primary opens a position — fallback goes silent (or closes). When primary is idle — fallback trades at a reduced position (dual_size). Priority is unconditional: primary always displaces fallback.

Strategies for Examples

Throughout the series we used three strategies. Here are their parameters for the 750-day period:

| Parameter | Strategy A | Strategy B | Strategy C |

|---|---|---|---|

| PnL | +55% | +27% | +300% |

| Trades | ~500 | ~40 | ~400 |

| Trading time | ~15% | ~5% | ~45% |

| MaxDD | ~0.9% | ~0.75% | ~17% |

| PnL/active day | 0.49%/d | 0.72%/d | 0.89%/d |

| Character | Medium activity | Rare, high conviction | Frequent, aggressive |

As we showed in PnL per Active Time, ranking by raw PnL and by PnL/active day produces different results. For cascade orchestration, the second metric is what matters.

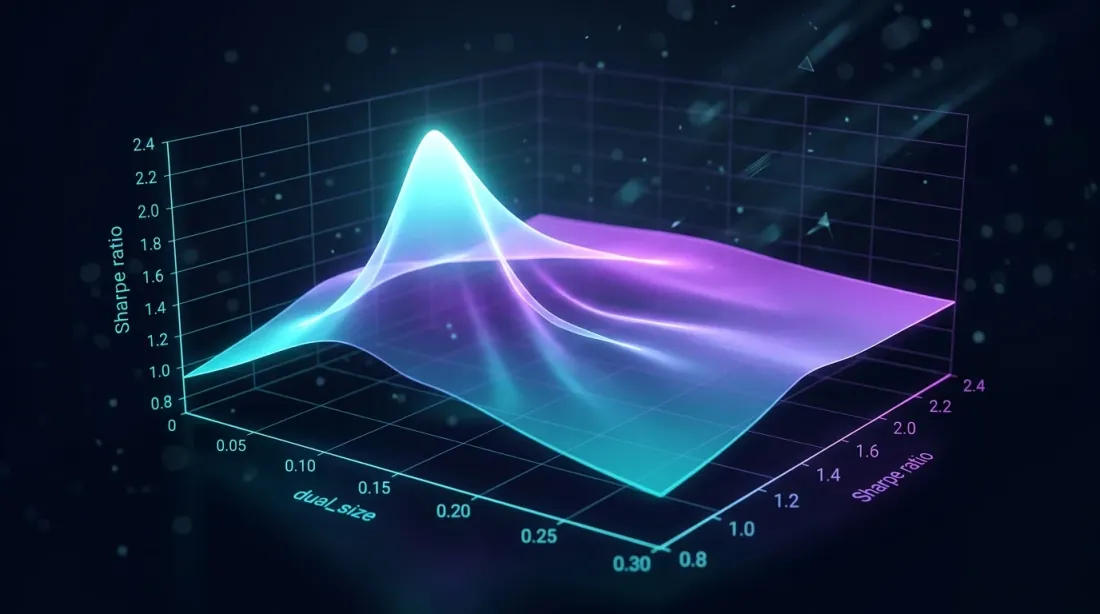

Optimal dual_size

Grid search over dual_size reveals a Sharpe ratio peak — too large increases drawdown, too small wastes idle time

Grid search over dual_size reveals a Sharpe ratio peak — too large increases drawdown, too small wastes idle time

The Selection Problem

dual_size is the fraction of the full position that the fallback strategy receives. It is the key cascade parameter:

-

Too large (e.g., 0.5 = 50%): when primary and fallback are active simultaneously, total exposure = 150% of target. Drawdown doubles. Loss-profit asymmetry makes this disproportionately expensive.

-

Too small (e.g., 0.01 = 1%): fallback fills 85% of idle time but earns pennies. Capital effectively sits idle.

-

Optimal: fallback contributes meaningful PnL without critically increasing drawdown during simultaneous operation with primary.

Formalization

Let:

- — primary PnL per unit of time

- — fallback PnL per unit of time

- — fraction of time in position (primary)

- — fraction of time in position (fallback)

- — dual_size (0..1)

- — fraction of time when both are in position

Total cascade PnL:

Total MaxDD (worst case — full correlation):

If we constrain total drawdown to :

Grid Search

In practice, the optimal dual_size is found via grid search on the cascade backtest:

import numpy as np

from dataclasses import dataclass

@dataclass

class CascadeResult:

dual_size: float

total_pnl: float

max_dd: float

sharpe: float

pnl_per_active_day: float

def grid_search_dual_size(

primary_equity: np.ndarray, # equity curve primary (minute bars)

fallback_equity: np.ndarray, # equity curve fallback (minute bars)

primary_positions: np.ndarray, # 1 = in position, 0 = flat

fallback_positions: np.ndarray,

grid: np.ndarray = np.arange(0.01, 0.30, 0.005),

) -> list[CascadeResult]:

"""

Grid search for dual_size.

primary_equity and fallback_equity are log-returns, minute bars.

"""

results = []

for d in grid:

fallback_active = fallback_positions & ~primary_positions

cascade_returns = (

primary_equity * primary_positions

+ d * fallback_equity * fallback_active

)

equity_curve = np.cumprod(1 + cascade_returns)

peak = np.maximum.accumulate(equity_curve)

drawdown = (equity_curve - peak) / peak

max_dd = drawdown.min()

total_pnl = equity_curve[-1] - 1

sharpe = (

np.mean(cascade_returns) / np.std(cascade_returns)

* np.sqrt(525_600) # minutes per year

) if np.std(cascade_returns) > 0 else 0

active_minutes = np.sum(primary_positions | fallback_active)

active_days = active_minutes / (24 * 60)

pnl_per_day = total_pnl / active_days if active_days > 0 else 0

results.append(CascadeResult(

dual_size=d,

total_pnl=total_pnl,

max_dd=max_dd,

sharpe=sharpe,

pnl_per_active_day=pnl_per_day,

))

return sorted(results, key=lambda r: r.sharpe, reverse=True)

Typical optimum for crypto strategies: dual_size in the range 0.05-0.10 (5-10% of full position). With Strategy B as primary (MaxDD 0.75%) and Strategy A as fallback (MaxDD 0.9%):

The drawdown constraint is not binding — the optimum is determined by cascade Sharpe. In practice, grid search typically yields (6.8%).

Score-Based Allocation

Strategies ranked by composite score — confidence adjustment penalizes small samples, funding costs reduce net edge

Strategies ranked by composite score — confidence adjustment penalizes small samples, funding costs reduce net edge

When there are more than two strategies, cascade generalizes to score-based allocation.

Ranking by PnL per Active Time

As described in detail in PnL per Active Time, the strategy score is calculated accounting for:

- PnL per active day — capital utilization efficiency

- Confidence adjustment — penalty for small samples (t-distribution)

- Funding costs — real cost of leverage (Funding rates)

- MaxLev — scaling with drawdown consideration (Loss-profit asymmetry)

Confidence Adjustment for Rare Strategies

Strategy B with 40 trades requires a serious penalty. We use the lower bound of the confidence interval:

import scipy.stats as st

import numpy as np

def confidence_factor(trade_returns: np.ndarray, confidence: float = 0.95) -> float:

"""Confidence factor: 0..1, penalty for small samples."""

n = len(trade_returns)

if n < 10:

return 0.0

mean_r = np.mean(trade_returns)

if mean_r <= 0:

return 0.0

se = np.std(trade_returns, ddof=1) / np.sqrt(n)

t_crit = st.t.ppf(1 - (1 - confidence) / 2, df=n - 1)

ci_lower = mean_r - t_crit * se

return max(0.0, ci_lower / mean_r)

cf_b = confidence_factor(np.random.normal(0.0067, 0.028, 40))

cf_a = confidence_factor(np.random.normal(0.0011, 0.008, 500))

Funding Cost Integration

On perpetual futures, funding is paid every 8 hours. With leverage and average rate :

For Strategy A with MaxLev = 55x and average funding rate 0.01%:

With PnL/active day = 0.49%, net PnL is negative: /day. The strategy is unprofitable at full leverage. Detailed analysis in Funding Rates Kill Your Leverage.

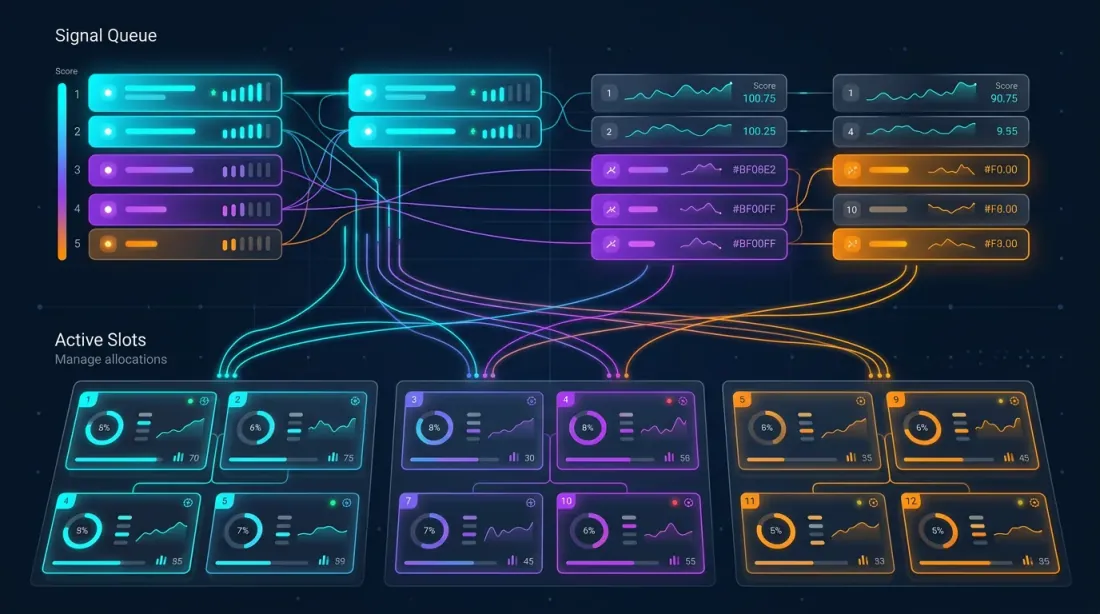

Multi-Strategy Orchestrator

Architecture

The orchestrator manages strategies on trading pairs. Total number of potential positions: . But capital is limited — no more than simultaneous positions (slots) are allowed.

┌─────────────────────────────────────────────┐

│ ORCHESTRATOR │

│ │

│ Signal Queue (sorted by score): │

│ ┌──────────────────────────────────────┐ │

│ │ 1. Strategy C × ETHUSDT score=223 │ │

│ │ 2. Strategy B × BTCUSDT score=142 │ │

│ │ 3. Strategy A × SOLUSDT score=100 │ │

│ │ 4. Strategy C × BTCUSDT score=89 │ │

│ │ 5. Strategy A × ETHUSDT score=76 │ │

│ └──────────────────────────────────────┘ │

│ │

│ Active Slots (max_parallel = 3): │

│ ┌──────────────────────────────────────┐ │

│ │ Slot 1: Strategy C × ETHUSDT [FULL] │ │

│ │ Slot 2: Strategy B × BTCUSDT [FULL] │ │

│ │ Slot 3: Strategy A × SOLUSDT [DUAL] │ │

│ └──────────────────────────────────────┘ │

│ │

│ Conflict Rules: │

│ - One position per pair │

│ - Primary displaces fallback on same pair │

│ - Higher score wins for cross-pair slots │

└─────────────────────────────────────────────┘

Slot Management

from dataclasses import dataclass, field

from enum import Enum

from typing import Optional

import heapq

import time

class SlotType(Enum):

FULL = "full" # primary strategy, 100% position

DUAL = "dual" # fallback strategy, dual_size position

@dataclass

class Signal:

strategy_id: str

pair: str

direction: str # "long" | "short"

score: float

is_primary: bool # primary or fallback

timestamp: float

@dataclass(order=True)

class Slot:

"""A single orchestrator slot."""

priority: float = field(compare=True) # negative score for min-heap

strategy_id: str = field(compare=False)

pair: str = field(compare=False)

slot_type: SlotType = field(compare=False)

entry_time: float = field(compare=False)

class Orchestrator:

"""

Multi-strategy orchestrator with cascade mode.

Manages N strategies x M pairs within max_parallel_positions slots.

Primary strategies have unconditional priority over fallback.

"""

def __init__(

self,

max_parallel_positions: int = 10,

dual_size: float = 0.068,

min_score: float = 0,

):

self.max_parallel = max_parallel_positions

self.dual_size = dual_size

self.min_score = min_score

self.active_slots: dict[str, Slot] = {} # pair -> Slot

self.pending_signals: list[Signal] = []

def on_signal(self, signal: Signal) -> Optional[dict]:

"""

Process a new signal. Returns an action or None.

Actions:

- {"action": "open", "pair": ..., "size": ..., "slot_type": ...}

- {"action": "replace", "pair": ..., "close_strategy": ..., "open_strategy": ...}

- None (signal rejected)

"""

if signal.score < self.min_score:

return None

pair = signal.pair

if pair in self.active_slots:

existing = self.active_slots[pair]

if signal.is_primary and existing.slot_type == SlotType.DUAL:

self.active_slots[pair] = Slot(

priority=-signal.score,

strategy_id=signal.strategy_id,

pair=pair,

slot_type=SlotType.FULL,

entry_time=signal.timestamp,

)

return {

"action": "replace",

"pair": pair,

"close_strategy": existing.strategy_id,

"open_strategy": signal.strategy_id,

"size": 1.0,

}

if signal.score > -existing.priority:

slot_type = SlotType.FULL if signal.is_primary else SlotType.DUAL

size = 1.0 if signal.is_primary else self.dual_size

self.active_slots[pair] = Slot(

priority=-signal.score,

strategy_id=signal.strategy_id,

pair=pair,

slot_type=slot_type,

entry_time=signal.timestamp,

)

return {

"action": "replace",

"pair": pair,

"close_strategy": existing.strategy_id,

"open_strategy": signal.strategy_id,

"size": size,

}

return None # existing has higher priority

if len(self.active_slots) < self.max_parallel:

slot_type = SlotType.FULL if signal.is_primary else SlotType.DUAL

size = 1.0 if signal.is_primary else self.dual_size

self.active_slots[pair] = Slot(

priority=-signal.score,

strategy_id=signal.strategy_id,

pair=pair,

slot_type=slot_type,

entry_time=signal.timestamp,

)

return {

"action": "open",

"pair": pair,

"strategy": signal.strategy_id,

"size": size,

"slot_type": slot_type,

}

worst_pair = min(

self.active_slots,

key=lambda p: -self.active_slots[p].priority,

)

worst_slot = self.active_slots[worst_pair]

if signal.score > -worst_slot.priority:

del self.active_slots[worst_pair]

slot_type = SlotType.FULL if signal.is_primary else SlotType.DUAL

size = 1.0 if signal.is_primary else self.dual_size

self.active_slots[pair] = Slot(

priority=-signal.score,

strategy_id=signal.strategy_id,

pair=pair,

slot_type=slot_type,

entry_time=signal.timestamp,

)

return {

"action": "replace",

"pair": pair,

"close_strategy": worst_slot.strategy_id,

"close_pair": worst_pair,

"open_strategy": signal.strategy_id,

"size": size,

}

return None # all active slots have higher scores

def on_exit(self, pair: str) -> None:

"""Strategy closed a position."""

if pair in self.active_slots:

del self.active_slots[pair]

def utilization(self) -> float:

"""Current slot utilization."""

return len(self.active_slots) / self.max_parallel

def fill_efficiency_snapshot(self) -> float:

"""Weighted utilization: FULL=1.0, DUAL=dual_size."""

total = sum(

1.0 if s.slot_type == SlotType.FULL else self.dual_size

for s in self.active_slots.values()

)

return total / self.max_parallel

Conflict Resolution

Three levels of conflict:

Level 1 — Same pair, same direction. The strategy with the higher score wins. If both are primary — score determines the winner. If one is primary and the other fallback — primary wins unconditionally.

Level 2 — Same pair, opposite direction. Prohibited: you cannot simultaneously be long and short on the same pair. The strategy with the highest score wins.

Level 3 — Cross-pair competition. When all slots are occupied, a new signal evicts the slot with the lowest score. This works as a priority queue.

Cascade Backtesting: Methodology

Joint simulation: primary and fallback equity curves with overlap zones and the combined cascade result

Joint simulation: primary and fallback equity curves with overlap zones and the combined cascade result

Why You Can't Just Sum PnL

The naive approach: backtest each strategy separately, sum the PnL. This produces an inflated result for three reasons:

-

Time overlap. When primary and fallback are active simultaneously, fallback should not trade (or trades at dual_size). Simple summing ignores this overlap.

-

Capital constraint. Total position is limited. If 5 strategies want to open simultaneously but there are only 3 slots — two strategies won't enter. Their PnL cannot be counted.

-

Transaction costs. Cascade switching (closing fallback, opening primary) generates additional commissions not present in individual backtests.

Joint Simulation

The correct cascade backtest is a joint simulation of all strategies on a shared timeline:

import numpy as np

from typing import NamedTuple

class Trade(NamedTuple):

strategy: str

pair: str

entry_time: int # minute index

exit_time: int # minute index

pnl_per_minute: float # log-return per minute

is_primary: bool

score: float

def backtest_cascade(

all_trades: list[Trade],

total_minutes: int,

max_slots: int = 10,

dual_size: float = 0.068,

switch_cost: float = 0.0006, # 0.06% round-trip

) -> dict:

"""

Joint simulation of cascade portfolio.

Walk through each minute, apply orchestrator rules,

calculate PnL accounting for overlap and slot constraints.

"""

entries = {}

exits = {}

active_trades = {} # trade_id -> Trade

for i, trade in enumerate(all_trades):

entries.setdefault(trade.entry_time, []).append((i, trade))

exits.setdefault(trade.exit_time, []).append((i, trade))

active_slots = {} # pair -> (trade_id, SlotType)

equity = np.ones(total_minutes)

switch_costs_total = 0.0

for t in range(1, total_minutes):

for trade_id, trade in exits.get(t, []):

if trade.pair in active_slots:

slot_id, _ = active_slots[trade.pair]

if slot_id == trade_id:

del active_slots[trade.pair]

new_signals = sorted(

entries.get(t, []),

key=lambda x: x[1].score,

reverse=True,

)

for trade_id, trade in new_signals:

pair = trade.pair

if pair in active_slots:

existing_id, existing_type = active_slots[pair]

existing_trade = all_trades[existing_id]

if trade.is_primary and existing_type == SlotType.DUAL:

active_slots[pair] = (trade_id, SlotType.FULL)

switch_costs_total += switch_cost

continue

if trade.score > existing_trade.score:

slot_type = SlotType.FULL if trade.is_primary else SlotType.DUAL

active_slots[pair] = (trade_id, slot_type)

switch_costs_total += switch_cost

elif len(active_slots) < max_slots:

slot_type = SlotType.FULL if trade.is_primary else SlotType.DUAL

active_slots[pair] = (trade_id, slot_type)

minute_return = 0.0

for pair, (trade_id, slot_type) in active_slots.items():

trade = all_trades[trade_id]

size = 1.0 if slot_type == SlotType.FULL else dual_size

minute_return += trade.pnl_per_minute * size

equity[t] = equity[t - 1] * (1 + minute_return)

peak = np.maximum.accumulate(equity)

max_dd = ((equity - peak) / peak).min()

total_pnl = equity[-1] - 1 - switch_costs_total

return {

"total_pnl": total_pnl,

"max_dd": max_dd,

"switch_costs": switch_costs_total,

"equity_curve": equity,

}

Transaction Cost on Switching

Each cascade switch (fallback -> primary) requires:

- Closing the fallback position: taker fee (0.04% on Binance futures)

- Opening the primary position: taker fee (0.04%)

- Spread: ~0.01-0.02%

Total switch cost: ~0.06-0.10% per switch. With 100 switches over the period:

This is a significant amount. A cascade with frequent switching can underperform a single strategy due to transaction costs.

Multi-Pair Extension: N Strategies on M Pairs

Network of N strategies connected to M trading pairs — correlation strength determines effective diversification

Network of N strategies connected to M trading pairs — correlation strength determines effective diversification

Combination Space

3 strategies on 10 pairs = 30 potential signals. With max_slots = 5, the orchestrator selects the top 5 by score. This is a combinatorial problem: possible portfolios at each moment.

In practice, a greedy algorithm (sort by score, fill top-down) produces near-optimal results in .

Correlation Between Pairs

Crypto pairs are strongly correlated. BTC drops — ETH, SOL, AVAX drop together. This means 5 long positions on 5 different pairs are effectively one large position on the "crypto market."

As we analyzed in detail in Signal Correlation, the effective number of independent positions:

where is the average correlation between pairs.

With and :

Five positions on correlated pairs are equivalent to 1.3 independent positions. Diversification is virtually absent.

Practical Implications for Cascade

def effective_diversification(

positions: list[dict], # [{"pair": "BTCUSDT", "direction": "long"}, ...]

correlation_matrix: np.ndarray,

pair_index: dict[str, int],

) -> float:

"""

Calculate effective diversification of open positions.

Returns:

N_eff / N — diversification coefficient (0..1)

"""

n = len(positions)

if n <= 1:

return 1.0

total_corr = 0.0

pairs_count = 0

for i in range(n):

for j in range(i + 1, n):

idx_i = pair_index[positions[i]["pair"]]

idx_j = pair_index[positions[j]["pair"]]

rho = correlation_matrix[idx_i, idx_j]

if positions[i]["direction"] != positions[j]["direction"]:

rho = -rho

total_corr += rho

pairs_count += 1

avg_rho = total_corr / pairs_count if pairs_count > 0 else 0

n_eff = n / (1 + (n - 1) * max(0, avg_rho))

return n_eff / n

The orchestrator should account for correlation when filling slots. Two options:

- Diversification bonus: when ranking, add a bonus to the score of strategies on uncorrelated pairs.

- Correlation cap: limit the number of same-direction positions on correlated pairs.

Cascade Optimization Pipeline

Eight connected stages from data preparation through validation to live orchestration — each builds on the previous

Eight connected stages from data preparation through validation to live orchestration — each builds on the previous

The full pipeline from data to production consists of 8 stages:

Stage 0: Data Preparation

Load historical data, build Parquet cache for multi-timeframe access. Without efficient caching, subsequent stages are unacceptably slow.

Stage 1: TF + Length (Hill-Climbing Grid)

Select the base timeframe and indicator window lengths. Coarse grid: TF from {1m, 5m, 15m, 1h, 4h}, Length from {10, 20, 50, 100, 200}. Hill-climbing from the best grid point.

Stage 2: Separation (Coordinate Descent, 12 Parameters)

Optimize separation parameters (entries/exits). Coordinate descent over 12 parameters — indicator thresholds, filters, stop-losses, take-profits. Coordinate descent is cheaper than Optuna for high-dimensional deterministic objective functions.

Stage 3: Meta-Parameters (Coordinate Descent)

Meta-parameters: max hold time, min PnL for exit, trailing stop configuration. Again coordinate descent. Check robustness via plateau analysis — if the optimum is point-like, the strategy is over-optimized.

Stage 4: Combo Optimization

Grid search over pairs (Primary, Fallback). For each combination: select dual_size, calculate cascade PnL via joint simulation.

Stage 5: Validation

Multi-level validation:

- Multi-symbol: strategy tested on 10+ pairs, not just the optimization pair

- Walk-forward: sliding IS/OOS window

- Parameter stability: plateau analysis at each stage

- Monte Carlo bootstrap: confidence intervals for cascade PnL

- Backtest-live parity: comparison of backtest with paper trading

Stage 6: Ranking and Selection

Rank cascade combinations by score. Top-K combinations advance to Stage 7. Score accounts for confidence adjustment, funding costs, and fill_efficiency.

Stage 7: Orchestration

Final stage: launch the orchestrator on strategies and pairs in cascade mode. Slot management, priority queue, conflict resolution — everything described above.

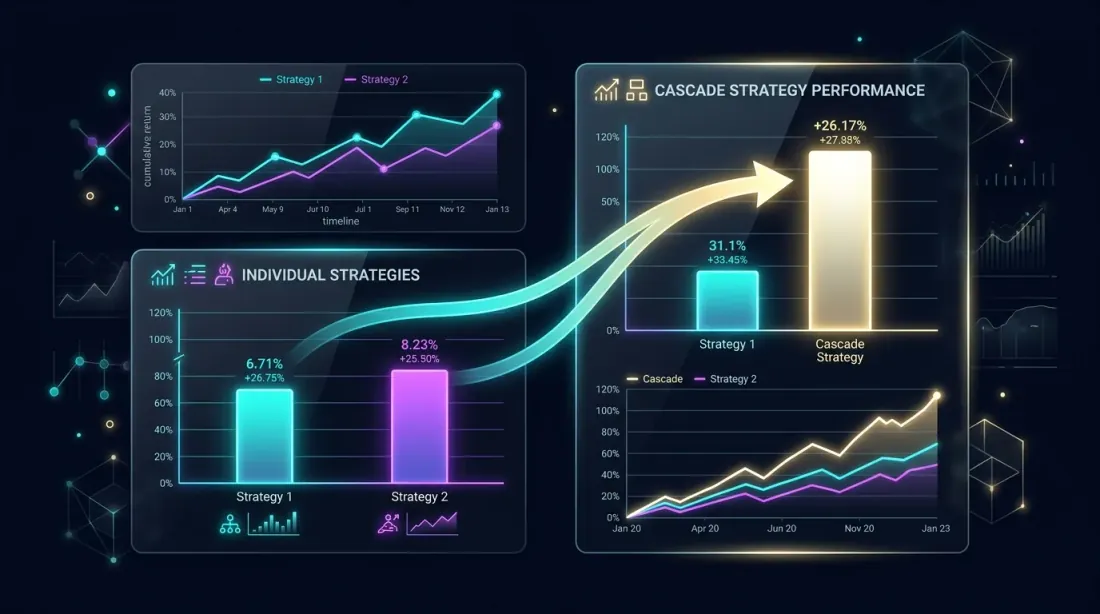

Performance Analysis: Cascade vs. Individual

Side-by-side comparison: cascade portfolio outperforms individual strategies through idle time utilization

Side-by-side comparison: cascade portfolio outperforms individual strategies through idle time utilization

Theoretical Cascade Advantage

Suppose primary trades of the time with PnL/day = 0.49%. Fallback trades with PnL/day = 0.89%. Overlap = (assuming independence).

Primary alone (Strategy A):

Cascade (A primary + C fallback):

Cascade gain: +31% to PnL from fallback, with minimal drawdown increase ( added to MaxDD).

When Cascade Doesn't Help

Cascade is ineffective when:

- Primary is active >80% of the time. Little idle time — nowhere for fallback to fit in.

- Strategies are highly correlated. Primary and fallback generate signals simultaneously — overlap is high, and fallback is idle precisely when primary is also idle.

- Switch costs exceed fallback PnL. With frequent switching, cascade commissions eat fallback profits.

- dual_size is too small. At , fallback earns 1% of its potential — below commissions.

Comparison Table

| Configuration | Annual PnL | MaxDD | Sharpe | Switch costs |

|---|---|---|---|---|

| Strategy A alone | 26.8% | 0.9% | 1.42 | 0 |

| Strategy C alone | 146.1% | 17% | 1.15 | 0 |

| Cascade A+C (d=0.068) | 35.2% | 2.06% | 1.58 | ~1.2% |

| Cascade B+A (d=0.068) | 19.4% | 1.36% | 1.71 | ~0.3% |

| 3-strategy orchestrator | 48.7% | 3.1% | 1.63 | ~2.1% |

Cascade A+C: primary A gains +8.4% from fallback C. Sharpe rises through idle time utilization. MaxDD grows moderately ().

Orchestration: fill_efficiency in Practice

Fill efficiency at ~78%: heatmap shows time utilization across strategies and pairs, bright cells indicate active trading

Fill efficiency at ~78%: heatmap shows time utilization across strategies and pairs, bright cells indicate active trading

The fill_efficiency parameter determines what fraction of idle time the orchestrator actually utilizes. As shown in PnL per Active Time, it can be estimated three ways:

- Fixed constant (0.80) — rough but universal

- Analytical estimate via — accounts for correlation

- Simulation from data — most accurate

For a cascade with 3 strategies on 10 pairs:

def cascade_fill_efficiency(

strategies: list[dict], # [{"trading_time": 0.15, "is_primary": True}, ...]

n_pairs: int = 10,

correlation_factor: float = 3.0,

) -> float:

"""Estimate fill_efficiency for a cascade portfolio."""

n_eff = n_pairs / correlation_factor

primary_times = [s["trading_time"] for s in strategies if s["is_primary"]]

p_primary = 1 - np.prod([(1 - t) ** n_eff for t in primary_times])

fallback_times = [s["trading_time"] for s in strategies if not s["is_primary"]]

p_fallback = 1 - np.prod([(1 - t) ** n_eff for t in fallback_times])

fill = p_primary + (1 - p_primary) * p_fallback

return min(fill, 1.0)

strategies = [

{"trading_time": 0.05, "is_primary": True}, # Strategy B

{"trading_time": 0.15, "is_primary": True}, # Strategy A

{"trading_time": 0.45, "is_primary": False}, # Strategy C as fallback

]

eff = cascade_fill_efficiency(strategies, n_pairs=10, correlation_factor=3.0)

Practical Recommendations

Six key recommendations for cascade deployment — from starting small to adaptive recalibration

Six key recommendations for cascade deployment — from starting small to adaptive recalibration

1. Start with Two Strategies

Don't launch 10 strategies on 20 pairs right away. Start with one primary + one fallback on 3-5 pairs. Make sure the joint simulation matches real behavior. Backtest-live parity is critical: if the cascade backtest diverges from live by even 5-10% — there's an error in orchestrator logic.

2. dual_size from Grid Search, Not Intuition

The optimal dual_size depends on the specific pair of strategies. 6.8% is a guideline, not a universal constant. Run grid search from 1% to 30% with 0.5% steps and select the Sharpe maximum.

3. Slot Limit Defines Architecture

With max_slots = 1, cascade degenerates into simple strategy switching. With max_slots = 50, the constraint is not binding and the problem reduces to an independent portfolio. The interesting zone: max_slots = 3-10, where slot management genuinely impacts results.

4. Account for Latency

In live trading, cascade switching is not instantaneous. Closing a fallback position + opening primary = 2 API calls + network latency + exchange matching. On a volatile market, the price can move in 200-500ms. Build in a slippage budget.

5. Monitor fill_efficiency

Track real fill_efficiency in production. If it is significantly lower than backtested — the orchestrator is not utilizing idle time as expected. Causes: API delays, rejected orders, margin constraints.

6. Use Adaptive Optimization

Cascade parameters (dual_size, score weights, slot limits) should not be static. Use adaptive drill-down for periodic recalibration on fresh data. The market changes — cascade parameters should follow.

"Backtests Without Illusions" Series: Summary

Complete system architecture: 13 interconnected modules from mathematics through validation to live orchestration

Complete system architecture: 13 interconnected modules from mathematics through validation to live orchestration

This article is the finale of a 13+ article series. Each article addressed one specific problem on the path from backtest to production. Here's how they connect:

Foundation: Return Mathematics

Loss-Profit Asymmetry — the multiplicative nature of returns, volatility drag, Kelly criterion. This is the mathematical foundation for everything that follows: why MaxDD determines leverage, why Sharpe matters more than raw PnL, why a 50% win rate with symmetric R:R is unprofitable.

Validation: Confidence Intervals and Robustness

Monte Carlo Bootstrap — turning a single-point estimate into a distribution with confidence intervals. Any metric (PnL, MaxDD, Sharpe) only makes sense with a confidence interval.

Walk-Forward Optimization — out-of-sample validation. A backtest on historical data is an IS result; WFO shows how the strategy performs on new data.

Plateau Analysis — parameter robustness check. If the optimum is point-like, the strategy is over-optimized.

Backtest-Live Parity — comparing backtest with real results. The final check before scaling.

Realistic Costs: Funding and Leverage

Funding Rates Kill Leverage — the hidden cost of leverage on perpetual futures. Without accounting for funding, a beautiful backtest turns into a loss.

Funding Rate Arbitrage — how to turn funding from an expense into a revenue source through cross-exchange strategies.

Metrics and Ranking

PnL per Active Time — the metric for ranking strategies in a portfolio. Raw PnL doesn't scale; PnL/active day does.

Signal Correlation — effective diversification in a portfolio of correlated pairs.

Infrastructure and Optimization

Parquet Cache for Multi-Timeframe Backtests — data infrastructure for fast iterations.

Adaptive Drill-Down — adaptive optimization: coarse grid -> fine-tuning in promising zones.

Optuna vs. Coordinate Descent — optimizer selection: Optuna for low dimensions with noisy objectives, coordinate descent for high dimensions with smooth objectives.

Polars vs Pandas — DataFrame operation performance for backtesting.

Orchestration (This Article)

Cascade Strategies — combining all previous components into a working system. Score-based allocation uses PnL/active time, confidence adjustment, funding costs. Cascade mode fills idle time. Joint simulation validates the portfolio. Monte Carlo bootstrap provides confidence intervals for cascade PnL.

Each article is an independent module. Together they form a complete pipeline from data loading to live orchestration of a strategy portfolio.

Conclusion

Cascade is not the only approach to strategy portfolios. But it is one of the simplest and most practical: the primary strategy trades at full capacity, fallback fills idle time at a reduced position. Two key parameters (dual_size and max_slots) provide sufficient flexibility for most configurations.

Three takeaways:

-

Cascade must be backtested via joint simulation only. Summing individual PnL inflates results. Switch costs, overlap, slot constraints — all of this is only captured in joint simulation.

-

dual_size determines the PnL vs. drawdown trade-off. Typical optimum is 5-10%. Grid search on Sharpe is a reliable selection method.

-

The orchestrator is a score-based priority queue. Everything reduces to a single number (score) for each signal. Score = f(PnL/active day, MaxLev, confidence, funding). Strategies with the highest score get slots. The rest wait.

The "Backtests Without Illusions" series demonstrates one thing: between a beautiful backtest and real profit lie dozens of pitfalls. Each article removes one. Cascade orchestration is the last step: turning a set of validated strategies into a working portfolio.

Useful Links

- López de Prado — Advances in Financial Machine Learning: Portfolio Construction

- Pardo, R. — The Evaluation and Optimization of Trading Strategies

- Ernest Chan — Algorithmic Trading: Winning Strategies and Their Rationale

- Perry Kaufman — Trading Systems and Methods, Chapter on Portfolio Allocation

- Tomasini, Jaekle — Trading Systems: A New Approach to System Development and Portfolio Optimisation

- Bailey, D.H. & López de Prado — The Deflated Sharpe Ratio

- Markowitz, H. — Portfolio Selection (1952)

- Kelly, J.L. — A New Interpretation of Information Rate (1956)

Citation

@article{soloviov2026cascadestrategies,

author = {Soloviov, Eugen},

title = {Cascade Strategies: Priority Execution with Fallback Filling},

year = {2026},

url = {https://marketmaker.cc/ru/blog/post/cascade-strategies-orchestration},

version = {0.1.0},

description = {Finale of the "Backtests Without Illusions" series. How to build an orchestrator from N strategies x M pairs, implement cascade mode with priority and fallback filling, choose dual\_size, and why strategy portfolios cannot be backtested by summing PnL.}

}

MarketMaker.cc Team

Сандық зерттеулер және стратегия